Can You "Chargeback-Proof" a Transaction with 3-D Secure?

There are a lot of tools you can use to help prevent chargebacks resulting from criminal fraud. Take 3-D Secure, for example.

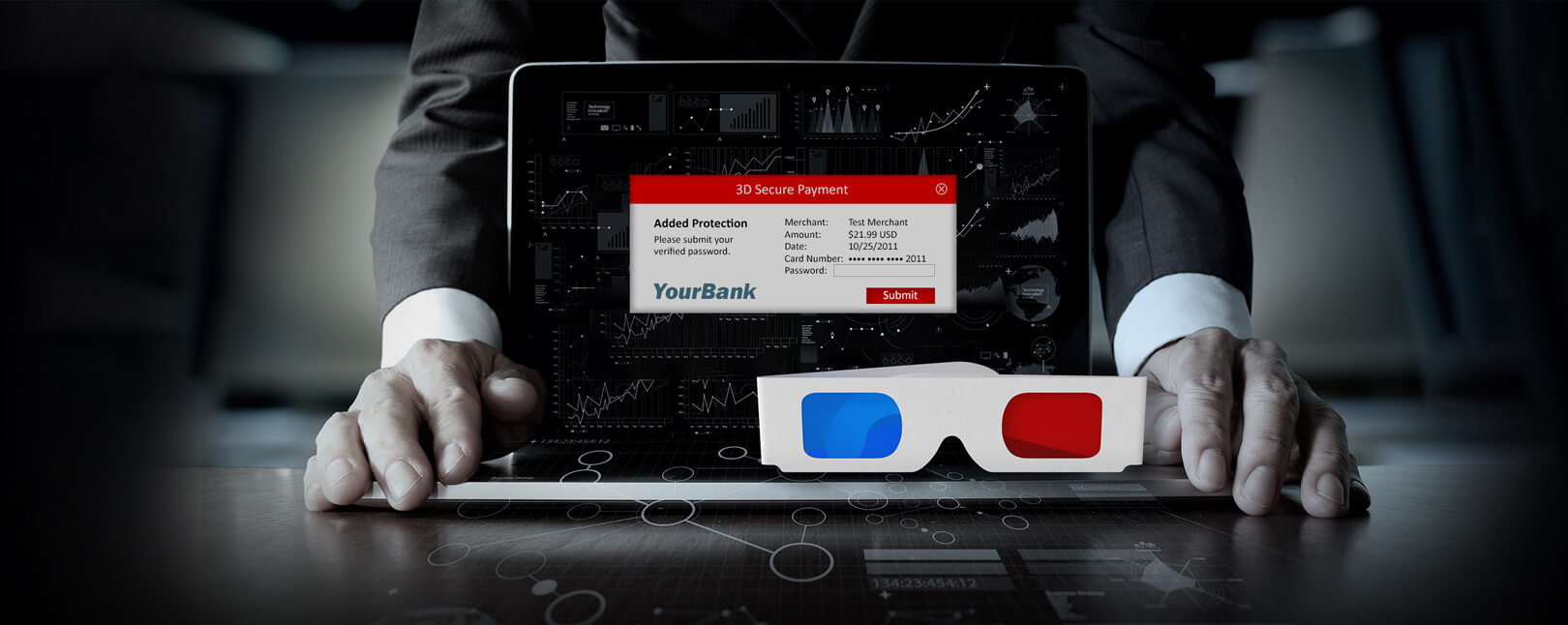

The 3-D Secure (3DS) platform works kind of like a PIN code, but for card-not-present transactions. When a cardholder attempts to complete a transaction, 3DS technology automatically directs the buyer to another page, asking them to provide an additional code. A genuine cardholder will be able to enter the unique code, but a fraudster would be unable to do so. This goes a long way to help prevent successful criminal fraud attacks.

It’s a great tool to have in your arsenal. However, the protection offered by 3-D Secure has let many merchants to slip into a false sense of security. Some have even come to think of 3-D Secure as a way to “chargeback-proof” their transactions. As we’ll see, though, it’s not quite that simple.

Does 3-D Secure Make a Transaction “Chargeback-Proof?”

The short answer is “no.” There are two reasons main for this:

1. The 3DS Adoption Rate Remains Low

First, 3-D Secure is an “opt-in” program. Your customer has to be enrolled in the 3DS platform that corresponds with the card brand in question (Verify by Visa, Mastercard SecureCode, etc.).

The use of 3DS in the transaction process increased by 79% over the past 18 months. A lot of merchants are embracing it for the first time, as the rollout of 3-D Secure 2.0 and subsequent updates have addressed many of the shortcomings that kept merchants on the fence with the technology. However, given that fewer than 1% of all credit & debit transactions processed in 2019 deployed the most recent version of 3DS, this suggests that adoption still remains very low. The majority of transactions initiated by cardholders still do not involve 3-D Secure verification.

2. The problem of chargeback sources

3DS provides protection against chargebacks filed using a “fraud” reason code. So, if a cardholder claims that a transaction was unauthorized and files a chargeback, but 3-D Secure technology was deployed, then you’re protected.

There are dozens of non-fraud reason codes to consider, though. You can still receive a chargeback if the cardholder, or the bank acting on the cardholder’s behalf, claims that you:

Submitted the wrong amount for the transaction total.

Submitted the transaction multiple times.

Failed to ship the merchandise in question.

Shipped goods that didn’t reflect what was promised.

Misrepresented the items sold.

That’s just to name a few potential scenarios. You can receive a chargeback tied to any number of claims and 3DS would not help, even if the claim is false.

There’s Only One Way to “Chargeback-Proof” Your Business.

Learn the secret to true chargeback prevention today.

Does 3-D Secure Prevent Chargeback Abuse?

Again, the answer is a resounding “no.”

Chargeback abuse, commonly known as friendly fraud, covers any situation in which a cardholder files a chargeback without a valid reason to do so. If the cardholder’s claim is not tied to a fraud reason code, the friendly fraud can still happen even if you deploy 3-D Secure.

To illustrate, let’s say a cardholder makes a purchase at your online store. You get a positive 3DS verification, receive authorization for the transaction, submit the transaction for processing, and ship the goods. Then, weeks later, the cardholder files a chargeback, claiming they never received the item. 3DS would be useless as evidence in this case because the cardholder’s claim has nothing to do with authorization.

[Tweet "Friendly fraud refers to any situation in which a cardholder files a chargeback without a valid reason to do so. 3DS has no effect on these false claims."]

Our internal data suggests that, by 2023, roughly six out of every ten chargebacks filed by cardholders will be friendly fraud. If we consider the scale of the problem, that leaves a lot of transactions unprotected. So, given the threat that chargeback abuse tied to non-fraud reason codes represents, you have to recognize that you’re still a long way from totally eliminating chargebacks.

Of course, we’re no saying that chargeback prevention is hopeless. We’re also not trying to say that 3DS is useless.

The technology offers great protection against criminal fraud chargebacks. But, instead of thinking about 3DS as a way to “chargeback-proof” your transactions, you should think about it as one component of a much larger engine that drives your fraud and chargeback management strategy.

4 Simple Steps to Prevent Chargebacks

You can think about chargeback management as a four-step process:

1. Identify Chargeback Sources

To reduce chargebacks, you must know the core cause behind each dispute. Reason codes won’t provide this information. It comes through detailed analysis, dynamic strategies, and innovative technologies.

We can trace all customer disputes back to one of three basic sources: merchant error, criminal fraud, or friendly fraud. Each of these represent a unique set of challenges and potential triggers, and each demands a unique prevention strategy. Once you know the sources of your chargebacks, you can deploy the right tools in the right manner to stop them.

The key to prevent criminal fraud chargebacks lies in building out a multilayer strategy to manage threat sources. 3-D Secure plays an important role here, but it’s just one of several tools to deploy, including:

…and more. You should collate the indicators generated from each transaction and subject them to fraud scoring. This lets you automatically approve or reject transactions based on the risk posed by known fraud indicators.

Here’s a shocking stat: somewhere between 20-40% of all chargebacks are caused by merchant error. That sounds bad, but it’s actually very good news. It means that these chargebacks are entirely preventable.

You have to conduct an in-depth, end-to-end evaluation of your business to prevent merchant error chargebacks, though. You must examine your policies and practices, reviewing and rewriting them as necessary, and evaluate every element of the sales process to pinpoint potential chargeback triggers.

Preventing chargebacks from friendly fraud is a challenge. It’s hard to anticipate or mitigate the threat using traditional prevention tactics because the abuse occurs after a transaction. The best approach is twofold:

First, deploy chargeback alerts and network inquiries to intercept disputes. These let you avoid chargebacks by refunding orders or providing additional transaction details to resolve inquiries. With these technologies in place, you never get caught off-guard by unexpected chargebacks.

To sum up, 3-D Secure is an important tool in your chargeback prevention arsenal. However, it’s just one of many.

You can use 3DS to prevent chargebacks with a “fraud” reason code if the cardholder is enrolled in the program. If the cardholder doesn’t use 3DS, or submits a chargeback claim tied to a non-fraud reason code, then 3DS can’t protect you.

You should think about 3DS as part of a larger strategy to protect yourself against disputes. Identifying chargebacks by source, and deploying the right tools to eliminate those threats, it the only way to truly chargeback-proof your operation.

Have other questions about chargeback prevention? Want to learn about other, more in-depth strategies to prevent chargebacks? Click below and learn more.

Like What You're Reading?Join our newsletter and stay up to date on the latest in payments and eCommerce trends.

Newsletter Signup

We’ll run the numbers; You’ll see the savings.Stop losing money to chargebacks. Let us show you how much you could save.

Please share a few details and we'll connect with you!

Over 18,000 companies recovered revenue with products from Chargebacks911