Chargebacks are forced payment reversals that banks initiate on behalf of cardholders. In this guide, we’ll share everything merchants need to know.

Explore the Chargebacks 101 Library

View article library

Chargebacks occur when a cardholder’s issuing bank forcibly reverses a debit or credit card transaction. When this happens, the funds are removed from the merchant’s account. In this article, we go through everything eCommerce sellers need to know about chargebacks. We’ll discuss how chargebacks work, when they’re appropriate for cardholders to file (and when they’re not), and how these reversals affect businesses.

Let’s say a consumer finds a charge on their credit card statement that they did not authorize. Or, maybe they did authorize a purchase, but are unhappy with the product or service once it arrived.

In both of these cases, the cardholder may have the option to dispute the charge with the bank that issued their card. If the bank feels the consumer’s claim is valid, the bank can reverse the payment using a process called a “chargeback.”

The chargeback process is a simple task for cardholders. But, it’s causing serious headaches for merchants. While well-intentioned, the chargeback process is antiquated and governed by rules that are often unevenly enforced. It’s easy to feel frustrated by the system.

In this article, we’ll explore how chargebacks work, where they came from, and how they have changed over time. We’ll also examine some of the consequences of chargeback misuse, and see what merchants can do to manage chargeback risk.

[noun]/* chärj • bak /

A chargeback is a credit or debit card charge that is forcibly reversed by an issuing bank. This typically happens after a cardholder claims a transaction was the result of fraud or abuse.

Chargebacks are the primary tool banks use to resolve credit card payment disputes. Cardholders benefit from the system, which acts as a shield against criminals or dishonest business practices. When misused, however, chargebacks can pose a serious threat to retailers, who stand to lose both revenue and business sustainability.

That can seem unfair to merchants. But, it’s important to note that chargebacks were created to act as a consumer safeguard. Chargebacks serve as protection from:

According to the 2024 Chargeback Field Report, as many as 70% of all chargebacks filed against merchants are fraudulent

Learn more about what chargebacks mean

Unlike refunds, in which merchants and cardholders work things out directly, chargebacks bypass the merchant entirely. Instead, the cardholder’s issuing bank steps in and forcibly reverses the transaction, leading to lost revenue, lost merchandise, and administrative fees for the seller.

With most refunds, the cardholder is obligated to return whatever was purchased to get their money back. Once the retailer receives the return, the customer receives the funds.

Filing a chargeback means the cardholder is attempting to bypass the merchant altogether by asking the bank to intervene. Successful disputes mean the merchant loses the revenue from the sale, plus the value of the merchandise. They’ll also forfeit any overhead costs like shipping, fulfillment, and interchange fees. Finally, the merchant is also billed an administrative fee for every chargeback.

Obviously, if the cardholder’s loss isn’t their fault, it’s reasonable for them to expect reimbursement. And if the blame lies with the merchant, then they should accept liability. As it turns out, however, a high proportion of chargebacks these days are being filed without a legitimate reason.

Learn about the difference between refunds & chargebacks

Cardholders can dispute both debt and credit card transactions. Credit cardholders are legally entitled to stronger legal protections, though in practice, most banks extend those same protections to debit cardholders, too.

Chargebacks can be used to dispute both debit and credit card transactions. That said, the card types differ in the level of fraud protection they offer users.

Credit cards offer consumers the widest fraud protection. By federal law, a cardholder can only be held liable for the first $50 of unauthorized transactions at most. Since the funds involved technically belong to the bank, not to the cardholder, anything beyond the $50 limit is the responsibility of the issuer.

Learn more about credit card chargebacks

In contrast, debit cards are tied to funds that actually exist in the cardholder’s account, rather than to a line of credit issued by the bank. Consumer liability for debit card fraud is legally capped at $50, but only if the bank is notified within two days of the loss. After that, cardholders could be responsible for up to $500 of losses, or even the total amount stolen.

Learn more about debit card chargebacks

Note, however, that these are only the minimums required by law. Banks are allowed to extend that protection. Most modern issuers offer zero liability on both debit and credit cards.

Chargeback protections were established under the Fair Credit Billing Act (FCBA) of 1974. Later legislation further elaborated on chargeback regulations.

In the early 1970s – before all the above protections had been put in place – bank credit cards had not yet gained widespread acceptance in the US. They existed, but consumers were hesitant to use them.

It wasn’t hard to steal these early cards and use them for unauthorized transactions. If that happened, the legitimate cardholder could easily get stuck with the liability for those bogus charges. The Fair Credit Billing Act of 1974 attempted to address these issues by creating chargebacks as we know them today.

Once these protections were in place, credit card use increased dramatically. Buyers saw that, for the most part, payment cards were safe to use. And, for a long time, comparatively few chargebacks were actually filed.

Learn more about the history of chargebacks

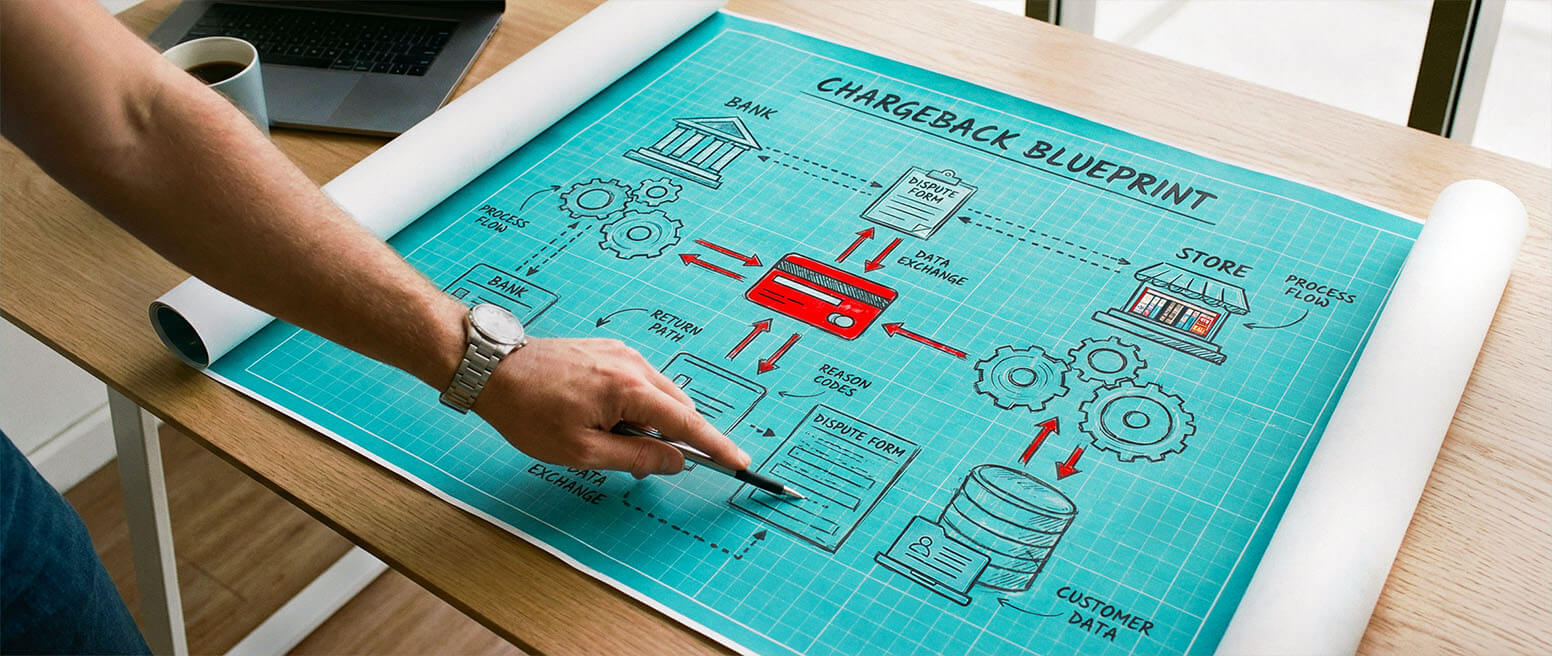

The chargeback process begins when the cardholder files a dispute with their bank. The issuer assigns a reason code and removes funds from the merchant’s account. The seller is usually allowed to re-present the transaction in response.

The number of steps involved in the chargeback process can vary based on multiple different factors, but the chargeback process generally works something like this:

Learn more about the chargeback process

It may seem like merchants are basically being judged “guilty until proven innocent” here. In truth, that’s more or less the case.

This becomes a major problem when it emerges that many chargebacks are issued by banks without a valid reason for the dispute. This isn’t a malicious act; in most cases, it’s because they’re not seeing the full picture. And the likely cause of that is the reason code system.

Chargeback reason codes are alphanumeric identifiers used by banks to explain the cause of a dispute. However, they often fail to capture the full context of a transaction.

Chargeback reason codes were created to standardize the list of acceptable reasons for the bank to file a credit or debit card chargeback on their customer’s behalf. To illustrate, say a cardholder decides to dispute a transaction. When the bank initiates the chargeback, they’ll attach a 2-to-4-digit alphanumeric code. That code corresponds to a list of acceptable chargeback reasons.

The codes themselves can be confusing, especially since each of the major card networks have their own specific set of codes. Payment service providers like Stripe or Paypal may also use unique indicators.

Plus, like we alluded to above, reason codes do not always tell the full story. In many cases, the reason code may be hiding an invalid customer claim (more on this later).

Learn more about chargeback reason codes

While uncommon, banks can — and do — file chargebacks on their own, even when they’re not prompted to do so by cardholders.

Most chargebacks happen because a cardholder initiates a dispute with their issuing bank online or over the phone. But, issuers aren’t passive order-takers, either. They can opt to initiate chargebacks on their own.

This can happen when banks detect transaction anomalies. For instance, purchases attempted with expired cards, duplicate transactions for the same order, incorrect currency codes, or evidence of merchant fraud. This results in a bank chargeback, which the issuer may initiate to protect themselves, as well as their cardholder.

From the merchant’s perspective, it’s identical to a standard chargeback. The transaction is forcibly reversed, funds are removed from the seller’s account, and the retailer is forwarded a chargeback reason code and given an opportunity to re-present it. The only notable difference is that the chargeback was initiated by the issuer, rather than the cardholder.

Learn more about bank chargebacks

Yes. Partial chargebacks allow cardholders to dispute a portion of a transaction, such as the cost of one missing item from a larger order.

Yes. While the practice is not common, there is such a thing as a partial chargeback. From the consumer’s perspective, this usually involves being happy with most of a purchase.

For example, let’s say a buyer ordered four items. Three were delivered on time, but the fourth never arrived. The cardholder may attempt to dispute just the cost of that missing item. This is what’s referred to as a partial chargeback request.

Merchants can use this option, as well. Going back to the above situation, let’s say the cardholder had attempted to dispute the entire purchase. The seller could re-present the cost of just the three items that were delivered, but accept the losses for the fourth item. If the bank feels the merchant’s claim is valid, they may only issue a partial chargeback.

Learn more about partial chargebacks

Cardholders can file chargebacks with their issuers online, in-app, over the phone, or in writing.

To initiate a chargeback, the cardholder must first dispute the transaction with the bank. Traditionally this has meant calling the number on the back of the credit card. More and more consumers, however, are opting to submit their dispute either online or through the issuer's mobile app.

It’s exceptionally easy for cardholders to file chargebacks. For convenience, most banks will include a link in their banking app that says “dispute this transaction” (or something to that effect) whenever a cardholder taps into their purchase history.

Cardholders can still call the number on the back of their cards, or even mail in a letter to file a dispute, if they choose to do so. Most won’t do this, though, as these methods are more cumbersome.

Once the ball is rolling, the process will go through the steps listed above, starting with the provisional credit to the buyer.

In most cases, card network rules require that cardholders first attempt to resolve the issue directly with the merchant before filing a chargeback. Some issuers may reject a chargeback claim if the cardholder cannot show they tried in good faith to work things out with the seller.

In most cases, cardholders have up to 120 days from the date of the original transaction to file a chargeback.Note that these timelines are comparatively generous — merchants, by contrast, have at most 45 days (and frequently as little as 5 to 10 days) to respond to a chargeback.

Learn how to dispute a credit card charge

All chargebacks stem from one of three basic sources: merchant error, third-party (“criminal”) fraud, or first-party (“friendly”) fraud.

Chargebacks can be grouped into three broad categories:

Billing, fulfillment, and delivery errors can trigger chargebacks. Luckily, these disputes are almost entirely preventable.

Merchants are financially responsible for the cost of unauthorized purchases from third parties. Fraud prevention and detection tools can help keep these disputes at bay.

The most common type of chargeback is also the most difficult to prevent because they stem from invalid disputes filed by cardholders themselves.

The first two categories, merchant error and criminal fraud, account for a minority of disputes (less than 10% and 20-40% of chargebacks filed, respectively). These two chargeback sources are mostly preventable because they stem from risks that merchants can mitigate or resolve.

For example, merchants can theoretically eliminate all merchant error chargebacks by elevating their customer service, relaxing their return policies, improving their inventory and order management processes, and auditing the performance of their logistics providers. Similarly, sellers can stop bad actors from attacking their businesses by hardening their account creation, login, and checkout workflows through better fraud detection technologies.

That leaves friendly fraud which, as mentioned earlier, accounts for a majority of chargebacks filed against merchants. Making matters worse is the fact that friendly fraud is notoriously difficult to detect at the point of sale because the transactions themselves are, in fact, valid: they’re authorized by the legitimate cardholder. It’s the chargeback — and the invalid rationale for it — that makes it fraudulent.

To say that merchants are entirely defenseless against friendly fraud, though, would be a misstatement. Sellers can incentivize chargeback-prone cardholders to reach out directly for refunds, and also deflect invalid disputes using chargeback alerts.

Learn more about chargeback sources

Cardholders can file legitimate chargebacks in cases of genuine fraud, missing shipments, damaged goods, or incorrect orders, and if they tried, but could not resolve the issue with the merchant.

Most accidents or innocent mistakes can be rectified with a simple call to the merchant. This is better for everyone: refunds are generally faster than filing a dispute, and the merchant avoids the costs of a chargeback. Merchants should cooperate with customers to resolve the issue. Of course, if the merchant isn't able or willing to work toward a mutually agreeable solution, a chargeback may be the only solution.

There are situations where cardholders have every right to file a chargeback. Some examples include:

Learn about reasons for disputing a charge

Cardholders can’t file chargebacks against legitimate transactions. Common reasons cardholders attempt this include dodging fees, circumventing return windows, buyer’s remorse, or trying to get things for free.

First-party chargeback misuse — colloquially termed “friendly fraud” — refers to situations in which customers dispute legitimate charges.

There are multiple ways a cardholder might file a chargeback inadvertently. For example, if the cardholder:

Of course, a cardholder may also file a chargeback, knowing that they should not have a right to do so. The chargeback is simply an attempt to “get something for free.” For example:

But, while friendly fraud can happen innocently or maliciously, the negative impact on the merchant is essentially the same.

Learn more about friendly fraud

Merchants who experience chargebacks incur steep administrative fees. They also risk being blacklisted by payment processors if their chargeback ratio rises beyond acceptable levels.

Chargebacks on credit cards have both short and long-term ramifications for merchants.

Each chargeback means the merchant is hit with a $20 to $100 fee. Even if the chargeback is later canceled, the fees and administrative costs still apply. Plus, if the consumer files a chargeback and simply keeps the merchandise, the merchant loses that revenue and any future potential profit.

There are long-term consequences to consider as well. If monthly chargeback rates exceed predetermined thresholds, excessive fines could be levied against the business. Plus, if chargeback rates remain above the acceptable threshold, the acquiring bank may simply terminate the merchant’s account.

If the merchant’s account is terminated, that business will be placed on the MATCH list. This means the business is blacklisted for at least five years, and will be unable to secure a standard merchant account with any processor or acquirer.

Learn more about chargeback costs

Merchants can fight bogus chargebacks through a process called chargeback representment. This is a formal, tightly-regulated process in which sellers can “re-present” transactions to the cardholder’s issuing bank in an effort to recover disputed funds.

To win a dispute in representment, merchants must present compelling evidence that aligns with the chargeback reason code received. For example, while proof of delivery from the carrier can be compelling evidence in an “item not received” claim, it may not be sufficient to counter an “item not as described” chargeback. In the latter case, photos or videos of the contents in the box prior to shipping may be more compelling.

Beyond gathering raw evidence, merchants will want to draft a chargeback rebuttal letter that summarizes the evidence submitted. Once all this information is compiled into a representment package, it should be submitted through the acquirer prior to the deadline.

Juggling evidence, rebuttal letters, timelines, reason codes, and ever-changing card network rules can be complex. That’s why enlisting the help of chargeback management professionals — like the experts at Chargebacks911® — can help you maximize your chargeback win rate.

Learn more about chargeback representment

Chargebacks are a real and growing threat for online merchants. They drain revenue, damage customer relationships, and can even threaten a merchant’s ability to process payments altogether.

The right chargeback prevention steps, however, can dramatically reduce disputes. In fact, preventing chargebacks may be the best thing one can do to increase revenue and ensure the long-term sustainability of an online business.

Merchants need to conduct a comprehensive overview of the tactics they deploy to prevent chargebacks and payment disputes. This includes fundamental strategies that are most effective at reducing chargebacks.

Learn more about chargeback prevention

eCommerce technology is constantly evolving, and new chargeback threats appear daily. An effective chargeback management strategy must be flexible enough to identify new trends and techniques, counteract new technology, and adapt on the fly to a shifting landscape.

No one understands this better than the experts at Chargebacks911® . That’s why we offer the most comprehensive chargeback management services and products available. Our transparent, end-to-end solutions go beyond prevention to revenue recovery and future growth.

Whatever you need to fight chargebacks, we can help. Contact us today for a free demo.

A chargeback is a credit or debit card charge that is forcibly reversed by an issuing bank. This typically happens after a cardholder claims a transaction was the result of fraud or abuse.

Chargebacks typically result from a cardholder claiming a transaction was the result of criminal fraud (identity theft, account takeover, etc.). The cardholder may also claim merchant abuse; being billed twice for the same item, for example.

The transaction amount will be temporarily taken from the merchant’s account and returned to the cardholder. The merchant can either contest or accept the claim.

If a merchant believes a chargeback is unwarranted, they can represent the claim to the issuer, along with compelling evidence to prove the transaction was valid. If the bank agrees with the evidence, the transaction amount will be returned to the merchant, less fees and administration costs.

For cardholders, the official answer is “no.” However, if there is an ongoing pattern of abuse, the merchant may refuse to do future business with you. Your bank could also suspend your account, which would hurt your credit.

No. However, deliberate chargeback fraud may be considered a form of credit card fraud or wire fraud. Legally speaking, that could theoretically result in jail time, although such incidents are rare.

No. Although the two are often used interchangeably, a refund is an equitable exchange; the customer returns the purchase in exchange for a price paid. With a chargeback, however, the merchant is likely to lose the purchase price, the wholesale cost of the item, shipping expenses, and other revenue.

Consumer chargebacks only apply to cases that involve criminal fraud (unauthorized purchases or identity theft), defective products (orders that come opened, or with parts missing; items that were significantly different advertised), or merchant misbehavior (incorrect or repeated charges on the account, or charges added to the bill after processing).