Pay by Bank: A Direct Consumer-to-Merchant Payment, With No Credit Card Required

In 2021, digital wallets were used to pay for nearly half (49%) of global online transactions. Surprising, right?

Widespread adoption of digital payment apps like Apple Pay makes sense. They’re easy, convenient, and are more secure than conventional card-not-present payments. Just one thing, however: digital wallet purchases are still tied to a payment card. That means merchants still incur interchange and other fees for every transaction processed.

If all those digital wallet transactions could just as easily be done without cards, retailers could save a fortune. That’s where the “pay-by-bank” method comes into play.

Recommended reading

- 7 Common Reasons Why Issuer Declines Happen

- Merchant Identification Number: How to Find Your Merchant ID

- My Bank Account is Under Investigation? What’s Going On?!

- VAR Sheets: Get All Your Documents Ready in 4 Basic Steps

- Internet Processing: Understanding the eCommerce Process

- Issuer vs Acquirer: What’s the Difference?

What is Pay by Bank?

- Pay by Bank

Pay by bank is a method of online payment that lets customers purchase goods and services by transferring funds directly from their bank account to the seller’s account.

[noun]/pā • bī • bangk/Most merchants have a “love-hate” relationship with plastic.

On the one hand, cards make it easier for consumers to conduct purchases. On the other hand, as much as 4% of every card purchase gets eaten up by interchange and other card processing fees.

Pay-by-bank transactions (sometimes called account-to-account payments) let the merchants bypass many of these fees. They use the automated clearinghouse system to transfer payments from a consumer’s checking account straight to the merchant’s. Much like a debit card, if the money isn’t in the cardholder’s account, the transaction is a no-go. If the funds are there, then the transfer takes place instantaneously.

For consumers, pay by bank offers convenience and security. And, with more and more shoppers already accustomed to alternate payment methods like mobile wallets, pay by bank doesn’t require much of a learning curve.

How Does Pay by Bank Work?

Moving money from one bank account to another isn’t a new concept, of course. Wire transfers and bank-to-bank transfers have been around for generations. More recently, peer-to-peer networks like Zelle have made instant transfers commonplace. Pay by bank is different, though.

P2P services involve a third-party app like Venmo or Cash App. Most have some type of limits, such as transfer amounts or locations. Plus, many of them charge a fee for their service.

Pay-by-bank systems bypass these problems by utilizing the open banking concept. This practice allows third-party financial service providers to access consumer banking data using an application programming interface (API). In simple terms, pay-by-bank technology lets bank account holders transfer funds through their bank app.

Qualifying merchants will need to enroll in the service, and shoppers will have to select the option at checkout. For the most part, though, consumers won’t notice much difference between pay by bank and a purchase conducted via Apple Pay or Google Pay. A typical pay-by-bank transaction goes like this:

Benefits of Pay by Bank

The convenience of pay by bank is a given for both consumers and retailers. Merchants get their money with no added fees, and shoppers will be able to see transactions in real-time, helping to prevent unauthorized charges or errors.

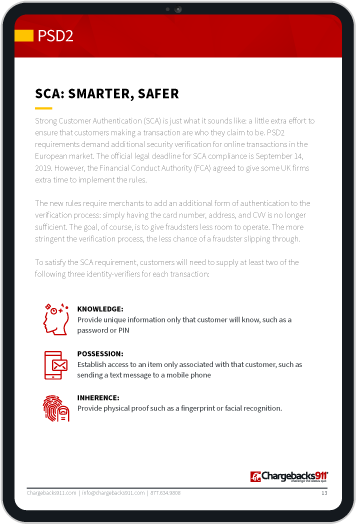

Security is strong, since the customer isn’t logging into a third-party account. Rather, they sign into their bank account using the same strong authentication (a combination of PIN, password, secure SMS text, biometric scan and so on) that their financial institution requires. With no additional apps involved, no account data is shared.

Whether you’re a bank, a merchant, or a consumer, transaction information is shared on a “need-to-know” basis. For example, the bank needs to know customer account data; the merchant doesn’t, and therefore has no access. Transactions are tokenized to further secure personal info.

Other benefits include less accounting, more accurate recordkeeping, and simplified fund tracking. This is good for consumers, obviously, but it’s also a boon to merchants as well, especially those using a recurring billing model. Unlike a credit or debit card, a bank account has no expiration date; thus, merchants don’t have to worry about failed transactions due to outdated information.

An often-overlooked benefit moving away from card transactions would be the elimination of physical waste. The payment card industry reportedly creates 6 billion new cards annually. That’s a lot of plastic that could be kept out of landfills.

For consumers, the pay-by-bank method is at least as fast and secure as using a credit card (usually more so on both counts). Let’s look at a side-by-side comparison:

| Security Feature | Open Banking | Credit Card Transaction |

| Customer Authentication | Strong (Two-Factor) | Card Number, CVV (Possibly Fraudulent) |

| Account Access Permission | Consumer Controlled | Issuer-Controlled |

| Fraud Protection | Real Time | Post-Transaction (Chargebacks) |

| Maximum Payment Limit | None (in Most Cases) | Issuer-Mandated Limit |

| Consumer Liability | Limited | Variable, Depending on Situation |

| Log-in Credentials | Customer & Bank Only | Shared With a Third-Party App |

| Requires | Bank Account | Approved Application |

The biggest draw for merchants is, again, the way these payments can lessen their dependence on the major card networks. According to the Neilson report, the eight largest credit card companies processed 136.88 billion transactions in 2022. This comes with a hefty price tag for merchants, when we consider that each of those transactions incurs interchange and other fees.

What About Fraud & Chargebacks?

For all the security protocols the card networks put in place, credit card fraud is still comparatively easy.

Cards can be dropped, copied, stolen, skimmed, or phished, with the fraudster disappearing before any crime is discovered. Compare that to pay by bank; even if a fraudster manages to swipe a phone, they would still need to unlock the device and the owner’s banking app, and provide all the necessary verification protocols before they could make a purchase.

There’s also the matter of chargebacks. In the US, the Fair Credit Billing Act protects consumers by limiting their liability should their card be used without their authorization. That’s all well and good, but consumers have learned how to “game” the system by filing invalid disputes (friendly fraud).

The chargeback system is not connected to pay by bank at all, which will decrease these instances of first-person abuse.

Fraud can't be prevented entirely. But, as a bank transfer, Pay by Bank is not covered by the laws that mandate the chargeback process.

Pay by bank could have a huge positive impact for merchants. They’ll save on card processing fees. They could also see a notable drop in chargebacks and first-party fraud.

Even so, credit cards are not going to disappear anytime soon. It’s important for merchants to consider a more comprehensive approach to fraud prevention and risk mitigation that can respond to the challenges they’re facing now.

Ready to learn about chargeback management that can work with both credit cards and all types of alternative payments? Talk to Chargebacks911® about a free chargeback analysis today.

FAQs

What is a pay-by-bank transfer?

Pay by bank is a method of online payment that lets customers purchase goods and services by transferring funds directly from their bank account to the seller’s account.

Is pay by bank open banking?

Yes. Pay by bank relies on open-banking practices to make direct transfers.

Is it safe to pay by bank transfer online?

Yes. Pay by bank is actually one of the safest ways to pay online. Since PBB only involves the consumer’s banking app, there are no 3rd-party access points or login data between the customer and the merchant. Banking apps require strong customer authentication, ensuring that all information is kept secure.

Is Zelle a bank transfer?

Yes and no. In the broader sense, Zelle does facilitate a transfer of money from one bank account to another. But it can only do so under certain conditions, such as both parties having a Zelle account. Pay by bank is a true bank transfer, however, as only the banks are involved in the process.