Merchant Identification Number: What is a MID & Why Does it Matter?

Ever wondered how the funds from a transaction make it from the cardholder’s bank to your merchant account? How do all the different players involved in a transaction make sure that money ends up in the right place?

Your merchant identification number, or “MID,” is a crucial factor. This code ensures that your money gets routed properly, and that no funds get lost in transit. That makes it an important part of the transaction reconciliation process.

Recommended reading

What is a Merchant Identification Number?

- Merchant Identification Number

A merchant identification number is a unique code provided to merchants by their payment processor. Often abbreviated as MID, this code is transmitted along with cardholder information to involved parties for transaction reconciliation. The MID can help identify a merchant when communicating with their processor and other parties.

[noun]/mər • CHənt • ī • den • tə • fə • kā • SHən • nəm • bər/Put simply, your MID is a code used to identify your merchant bank account. When you submit a cardholder’s information following a purchase, the MID is the number used to identify you throughout the transaction process. This helps ensure that the funds go to the correct account.

Without a MID tied to a transaction, the funds would have no destination. The bank would not be able to route the funds to you properly.

Can I Have Multiple MIDs?

Yes, you can have multiple MIDs at one time. But before we explain how this works, let’s cover a few different ID numbers that may be associated with your business, to make sure we’re clear on what we’re talking about.

Your MID uniquely identifies your business. That said, you might also have these identification numbers as well:

Gateway Identification Number

This number is assigned by the payment gateway and identifies your specific payment gateway account.

Terminal Identification Number (TID)

Assigned to individual payment processing devices, a TID is a unique number that identifies each physical payment processor and can be located on your payment processing equipment.

You have a unique TID for each of your card terminals. If you use three different card readers, each one has a unique TID. However, all of your terminals can still be grouped together under a single merchant identification number. In fact, you can even have multiple merchant accounts, but still group them under the same MID.

So, yes, you can have more than one MID, but a single merchant ID is generally enough for most businesses’ needs. Below, we’ll outline some situations in which multiple MIDs may be needed.

Why Would I Need Multiple MIDs?

Some merchants maintain multiple MIDs for accounting purposes. Businesses with multiple distinct sales channels, like restaurants, hotels, and multichannel retail, often have unique MIDs for different revenue streams. This helps separate and track where different revenue comes from.

As mentioned before, many businesses will only need one MID. That said, common examples in which a business might need multiple MIDs include:

In each of these cases, having unique MIDs for different parts of the business can simplify financial reporting and enhance operational efficiency. It can also provide clearer insights into the profitability and performance of each segment or service offering.

Do All Merchants Need a Merchant Identification Number?

No. Take Stripe, for instance; they're what's called a payment aggregator. This means that all Stripe merchants are basically sub-merchants under Stripe’s master merchant account. So, instead of each small business getting its own MID, they work under Stripe's account.

Services like Stripe, PayPal, and Square make payment processing a lot simpler for small businesses or solo entrepreneurs. These services handle all the tricky parts of dealing with banks and credit card companies for customers. This lets merchants start accepting payments without dealing with the complexities of conventional payments processing.

If you're a smaller business or just starting out, using one of these services can save you a lot of time. You get to use their systems and support, and you don't have to pay as much up front or go through the hassle of setting up your own merchant account.

For many small businesses, being under a payment aggregator's account is enough to get the job done. But, if your business is growing, sells in different markets, or you want more control over how you accept payments, then getting your own MID might be better.

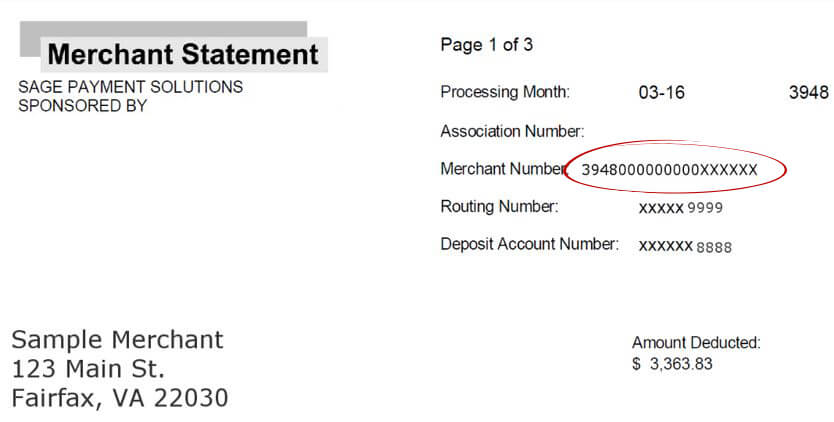

Locating Your Merchant ID

Is it possible to look up your merchant ID online?

No. Merchant IDs are not public information and cannot be found anywhere online. There is also no database or list you can view anywhere on the internet that will have this information.

That said, there are a few ways to view your MID. Your merchant identification number is:

#1 | The 15-digit code is located in the upper right-hand corner of your monthly merchant statement

#2 | On your credit card terminal, usually on a sticker or label

#3 | At the credit card receipts, before ‘terminal’

Your MID is a private number shared strictly between your business and payment processors. It’s just like an account number for a consumer bank. So, be sure to keep your MID secure, and never share it publicly.

What Do I Need to Acquire a MID?

When you're ready to acquire an MID, there's some specific information and documentation you'll need to provide. This is necessary for the financial institutions to verify your business and ensure compliance with regulatory standards.

Here's a breakdown of the key information you'll typically be asked for:

- 1. Taxpayer Identification Number (TIN): This is used for tax purposes and to confirm the legal standing of your business. Your TIN could be your business's Employer Identification Number (EIN) if you're incorporated, or your Social Security Number (SSN) if you're a sole proprietor.

- 2. Names of Principal Owners: You'll need to provide the full names and personal details of all the primary owners or key executives of the business. This often includes anyone with a significant stake in the company or those who have significant management responsibilities.

- 3. Business Legal Name & DBA (Doing Business As): The official legal name of your business as registered in your incorporation documents or business registration, along with any DBA names if you're operating under a different trade name.

- 4. Business Address & Contact Information: The physical location of your business (cannot be a P.O. Box), and your main contact details, such as phone number and email address.

- 5. Bank Account Information: Details of the business bank account where transactions will be deposited and fees will be withdrawn. This includes the bank's name, routing number, and account number.

- 6. Nature of Business: A description of what your business does, the types of products or services you sell, and your business model. This helps the processor understand the risk profile of your business.

- 7. Estimated Sales Volumes: Information on your expected monthly sales volumes and the average transaction size. This helps in setting up the correct processing limits for your account.

- 8. Website URL: For businesses that operate online or have an online sales component, you'll need to provide your website URL. This is so the processor can verify that your website complies with their requirements, such as displaying refund policies and contact information.

Gathering all this information before you start the application process can help streamline the acquisition of your MID. This will, in turn, ensure a smoother setup of your merchant services. Being prepared with detailed and accurate information also minimizes delays in the approval process. In other words, you can get up and running and start accepting payments more quickly.

Can I Lose My Merchant ID Number?

Again…the short answer is “yes.”

The most common reason businesses lose their merchant identification number is excessive chargebacks. It’s important to understand the different short- and long-term actions that can be taken against your account due to chargeback activity.

Withheld Funds

“The cash is secure…you just can’t have it.”

What is it

This describes the process that allows your processor to withhold a portion of transaction funds. This can be done for a variety of reasons; suspicious account activity is a common trigger, as is a sudden spike in chargeback volume.

How it Affects you

These funds can be held indefinitely while your processor investigates your situation. Your processor could also make this hold permanent in the form of a merchant account reserve. This is a common practice, especially for merchants in high-risk verticals. An ongoing merchant account reserve can be a rolling, capped, or up-front reserve, meaning some portion of your funds are always unavailable.

Processing Freeze

“Hitting ‘pause’ on your processing privileges.”

What is it

A processing freeze occurs when your processor temporarily shuts down your ability to accept card payments. This can happen if your chargeback ratio gets too close to the chargeback threshold outlined by the card scheme.

How it Affects you

Even with a hold on your account, you’ll still typically be able to accept new transactions. That’s not the case if your processor puts a freeze on your merchant ID. It’s a very serious matter for eCommerce merchants, as you have very few options available without credit or debit sales. You could accept payments via PayPal…but that’s about it while a processing freeze is in place.

Termination

“The end of the line.”

What is it

This is a pretty simple idea: your processor or acquirer sees you as more of a risk than an asset, so they cancel your merchant ID and close your account. This can be because of a clear or flagrant violation of the bank’s terms of service. More often, though, it’s because your chargeback ratio is consistently over the limit. You’re seeing regular, sustained chargeback activity above what the card scheme says is acceptable, and the bank refuses to cover for you any longer.

How it Affects you

As dangerous as a freeze is, at least there’s the prospect that it will eventually end. Not so with termination, unfortunately. If this happens, you’ll have to switch over to a high-risk processor, which means higher fees and more restrictions. That’s assuming your business survives, as you can’t accept any cards until you get a MID with a new processor and acquirer.

How Can I Protect My MID? Our Top 10 Tips to Keep Your Processing Privileges Secure

From fraud to data mishandling, there are a number of hiccups and other problems that can detail merchant processing. Naturally, protecting your business from theft, fraud, and other financial troubles is key to keeping your merchant identification number safe.

With that in mind, here are ten steps to help keep your MID secure:

Tip #1 | Boost Your Security Game

Use strong security measures for all payment-related activities. This means making sure all payment information is sent over secure, encrypted connections. Also, keeping your software updated and using firewalls and antivirus programs.

Tip #2 | Follow PCI-DSS Rules

Sticking to Payment Card Industry Data Security Standard requirements ensures you're doing everything you’re supposed to do in order to keep credit card info safe.

Tip #3 | Control MID Access

Only let trusted staff who need to handle payments or billing know your MID. Setting up roles in your team helps prevent misuse or accidental sharing.

Tip #4 | Watch Your Transactions

Keep an eye on your sales records for any odd or unauthorized transactions. Being vigilant will enable you to catch any misuse early and prevent fraud attacks that might jeopardize your MID.

Tip #5 | Choose Secure Payment Partners

Work with payment gateways and processors known for their top-notch security and fraud protection. Before signing up for service, inquire about any potential provider’s security standards and practices.

Tip #6 | Teach Your Team

Make sure your employees know how important it is to keep payment processes safe and how to spot and handle security threats. Provide ongoing training regarding security best practices and developing threats.

Tip #7 | Keep Your Contact Info Updated

Always update your contact details with your merchant service provider to get important account updates fast. Contact info mismatches could lead to your MID and other sensitive information falling into the wrong hands.

Tip #8 | Use Added Login Security

Add an extra step to your login process, like multi-factor authentication, to make accessing your merchant account and payment systems safer.

Tip #9 | Update Your Security

Always look for ways to make your security stronger, including keeping up with card network requirements and adapting to new technologies.

Tip #10 | Get Regular Security Checks

Have experts check your payment systems and security practices now and then. Many businesses recruit white-hat hackers to try and compromise their systems in order to spot weak spots and suggest how to fix them.

Following these steps can make a big difference in keeping your merchant identification number and other payment information safe. At the same time, prioritizing security shows your customers you're serious about protecting their data, which can help build trust.

That said, the above steps can’t resolve every problem you might encounter. Chargebacks are the foremost threat to your MID sustainability, and in many cases, chargebacks are not tied to true criminal activity.

Prevent Chargebacks to Protect Your MID

Chargebacks are the biggest threat to your merchant ID. That means the key to protecting your MID—and by extension, your entire business—is controlling chargebacks.

You have numerous tools at your disposal to prevent chargebacks due to criminal fraud, including:

That makes it sound rather simple. But, the fact is chargeback sources are extremely difficult to identify.

Our research shows that most chargebacks can ultimately be traced to friendly fraud, which relies on passing as a legitimate transaction. If you’re going to stop chargebacks and protect your MID, you’ll need a more comprehensive approach.

Want to ensure your merchant ID against friendly fraud, merchant error, and criminal fraud chargebacks? Continue below to get started today.

FAQs

How do I find a merchant ID number?

You can typically find your merchant ID number on your merchant account statements from your payment processor. You may also find it on your credit card terminal, usually on a sticker or label, or at the top of your credit card receipts, after the word “terminal.” If you're unable to locate it, contact your payment processor's customer service for assistance.

Is merchant ID the same as account number?

No, your merchant ID number is not the same as your bank account number. Your MID is a unique identifier for your merchant account used for payment processing, while your bank account number is used for banking transactions.

Is merchant ID the same as tax ID?

No, your Merchant ID number (MID) is different from your Taxpayer ID (TIN). Your MID is specific to your merchant payment processing activities, while your TIN is used for tax identification purposes with the IRS.

How do I create a merchant ID?

You can create a Merchant ID (MID) by applying for a merchant account through a bank or payment processing company. The provider in question will assign a unique MID to your business upon approval.

How much does it cost to open a merchant account?

The cost to open a merchant account varies widely, depending on the provider and your business type. It can include setup fees, monthly fees, transaction fees, and other charges. It's essential to consult with specific payment processors for detailed pricing tailored to your business needs.