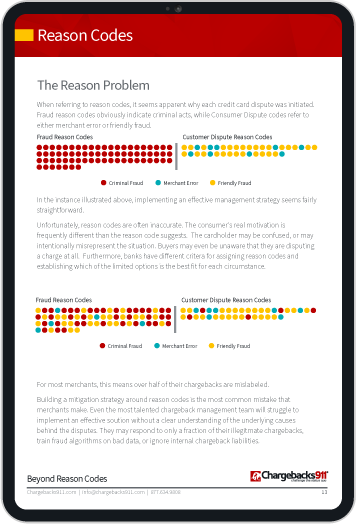

Explaining Pre-Compliance Chargebacks: Whatever Happened to Reason Code 98?

Every network has its own complex rulesets regarding disputes and chargebacks. Merchants understand that the chargeback system is a complex web of rules, counter-rules…and rule changes.

Networks constantly make changes and updates to this system. As a result, following the rules is sometimes easier said than done.

Even when a merchant believes they are in full compliance with one set… they could be breaking another. This is why it is essential for merchants to consistently monitor each network’s ever-changing rules and make every effort to comply.

Pre-compliance chargebacks were the banks’ response to broken rulesets that cost them time and revenue to correct. Later rule changes made this practice mostly obsolete, though, as we’ll get into with this article.

Recommended reading

- Visa Debit Chargebacks: Here’s Everything You Need to Know

- Visa Acquirer Monitoring Program: Major Updates to VAMP

- Visa Chargeback Time Limits: The 2024 Guide

- Visa Authorization Rules: Changes to Time Frames & Options

- Visa Chargeback Fees: 8 Tips to Help You Cut Dispute Costs

- Visa Resolve Online: The Guide to Manage Disputes With VROL

What is a Pre-Compliance Chargeback?

Previously, once a violation was discovered, the filing party was required to give the opposing member a chance to resolve the issue. This stage was called pre-compliance (hence the term “pre-compliance chargeback”).

These pre-compliance chargebacks were a Visa-specific network process. Banks used it to seek reimbursement from other banks when one broke those rules and caused a financial loss.

The idea was for members to work things out between themselves without the network’s input. If no resolution could be found, Visa would step in, review the available information, and decide which party bore final responsibility for the transaction. If the merchant was responsible, they could get hit with a dispute using Visa chargeback Reason Code 98.

Members were expected to comply with the network’s decision. An appeal process was available to members who disagreed with the network’s ruling, but the process was sluggish and costly, likely by design. Visa would prefer that disputes be resolved before they have to get involved.

Why Did Visa Eliminate Pre-Compliance Chargebacks?

So, how does reason code 98 affect the compliance process now? Simply put, it doesn’t...at least not anymore.

The whole point of pre-compliance was to provide dispute options in situations where there was no valid chargeback, representment, or arbitration right. Chargeback reason code 98 was used to describe any exception that fell into that category. In short, the bank didn’t have a clear, specific coding option to explain why it wanted to dispute a particular case.

With the implementation of Visa Claims Resolution, reason code 98 eventually became obsolete. Now, compliance cases must be submitted through Visa Resolve Online (VROL). Visa requires processors and banks use to this system for multiple tasks, including challenging initial chargeback results. The newer system is designed to make it easier and more straightforward to process and exchange dispute information.

Again, Visa prefers members use this data to resolve issues with no additional input from the network. To encourage members to use the Visa Resolution System, the network has since removed reason code 98 altogether.

What is Visa Chargeback Compliance?

To understand pre-compliance, we should define “compliance” in this context.

Visa created the compliance process as an alternative way to help resolve situations where one network member had violated internal network regulations. Compliance generally comes into play after a dispute has been addressed. One party disagrees with the outcome, but has no chargeback rights.

Questions about chargeback compliance? We’ve got the answers.

There are specific conditions under which the Visa compliance process can be initiated. All of the following must apply:

- A violation of the Visa Core Rules and Visa Product and Service Rules occurred.

- The violation is not covered by a specific dispute condition (reason code), representment, or pre-arbitration right.

- The network member incurred a financial loss resulting directly from the violation.

- The member would not have incurred the financial loss had the regulations been followed.

- The pre-compliance attempt to resolve was not accepted.

In simple terms, “compliance” claims are only an option if one party feels the other party didn’t play by the rules, leading to a loss of revenue for the filing member.

Compliance disputes can be handled by the issuing bank or the merchant’s processor. Issuers can initiate compliance claims against acquirers, and acquirers can file against issuers. It all depends on who committed the violation and the nature of the violation itself.

This type of case is outside the normal chargeback process, so it doesn’t affect the merchant’s chargeback ratio. While the damage was done with the original dispute, it won’t be assessed a second time.

What Are Visa Compliance Violations?

Numerous situations could meet all the criteria listed above—and thereby qualify as compliance violations. For example:

- The merchant continued to bill a cardholder without confirming that the transaction receipt's signature matched the card's signature.

- The cardholder agreed to be charged at least once, but the merchant billed for multiple key-entered transactions without the cardholder’s authority (card-present environment).

- A merchant/acquirer ignored a retrieval request for legal proceedings or law enforcement investigations.

- The Visa dispute processing system prevented a valid dispute because a member provided invalid transaction data.

The folks at Visa understand that merchants and banks make mistakes and sometimes break the rules when things get complicated. This is why the chargeback process exists in the first place: to regulate and correct these issues and prevent future problems (at least in theory). On the other hand, when cardholders break the rules, they’re generally committing criminal or friendly fraud.

The compliance process was implemented to address complications for which Visa does not have a predetermined, specified system.

How Pre-Compliance Chargebacks Affect Merchants

As stated above, pre-compliance chargebacks don’t affect a merchant’s chargeback ratio, which means they can never cause you to exceed any chargeback thresholds. Even though many pre-compliance chargebacks result from a regular chargeback, the pre-compliance portion is handled strictly by the acquiring and issuing banks. This means the merchant may only be charged for fees involved in the original transaction dispute.

That said, merchants should be aware that their actions may affect their relationship with their acquiring bank. This is true despite the fact that the compliance violations listed above would be handled at the banking level.

For example, if your business is constantly breaking the rules and incurring compliance violations that the bank must deal with, you should expect some repercussions. The bank may pass their fees down to you with additional penalties if you continue to break the rules. If the situation persists, they could even go as far as to limit or terminate your merchant account.

The good news is that with the advent of VROL, pre-compliance chargebacks are on their way out. Without reason code 98 to accommodate conflicts without defined dispute rights, banks don’t have much choice but to try to talk things out with each other.

This is probably a good outcome for everyone involved. It’s less of a burden on Visa, and it encourages more collaborative relations between member banks. Plus, merchants are always better off when fewer chargebacks are flying around.

However, this is no reason to become complacent. The merchant errors that led to reason code 98 chargebacks in the past can still cause problems that may come back to bite you.

Preventing Chargebacks is Better

Since pre-compliance cases are handled mainly by banks and processors, they shouldn’t be a merchant’s main focus—unless that merchant has broken the rules. In that case, they’ll need to review how the business handles card payments.

Generally speaking, the best chargeback approach is prevention. Although not all violations are identified from chargebacks, a chargeback can’t get to the compliance stage if it was never filed in the first place. That’s why a customized, multi-tiered chargeback mitigation strategy is so important.

Our experts at Chargebacks911® want to help you simplify the stress of confusing industry jargon. We can customize a sustainable chargeback prevention strategy for your business, backed by our exclusive ROI guarantee.

Want to learn more, or have other questions about the pre-compliance chargeback process? Contact us today.