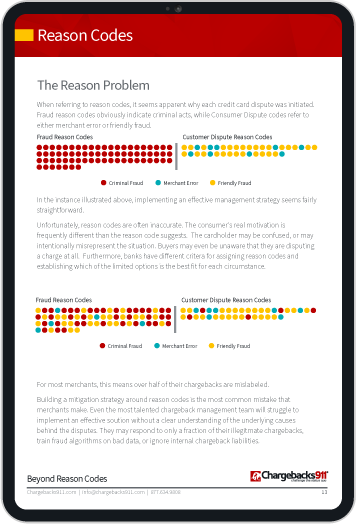

First-Party Fraud is an Epidemic. Is Compelling Evidence 3.0 the Cure?

It’s no secret that digital technologies and eCommerce are transforming retail. Reports show that the total transaction value in the digital payments segment is estimated to reach $3.53 trillion by 2027. That’s nearly double the amount projected for 2023.

The downside to this surge in digital purchasing is a matching rise in fraud activity. Specifically, first-party fraud, also known as “friendly” fraud.

First-party fraud refers to incidents in which consumers purposely supply the wrong information to try and get something for free. Unlike third-party fraud, there is no outside criminal involved here; the perpetrator is the cardholder.

The problem is reaching epidemic proportions. According to recent reports, around 19% of consumers consider first-party fraud “normal,” while 23% felt it was okay in certain scenarios. The situation is even more dire with younger buyers; one out of five Gen-Z consumers see no ethical problem with first-party. Over half admit they’d be fine with committing first-party fraud if there would be no negative consequences.

Clearly, the honor system isn’t working here, and it’s not just retailers who are paying the price. Community banks, payment processors, and online lending companies are also victims. Action is needed, but finding a solution can be tricky. After all, it’s hard to convince people to change when they don’t see their actions as a problem.

Recommended reading

- The Top 30 Chargeback Risk Factors to Eliminate in 2024

- Chargeback Insurance: Choose the Best Protection in 2024

- Can a Chargeback Blacklist Prevent Post-Transaction Fraud?

- What is a Business Continuity Plan? Tips, Guides & Examples

- How Stripe Chargeback Protection Defends Merchant Revenue

- Chargeback Protection: What are Your Options for 2024?

Evolving Policies are Needed

Card networks have recognized the problems caused by first-party misuse, and have rolled out new products to try and close loopholes in the system.

Verifi Order Insight and Ethoca Consumer Clarity, for instance, both provide means to detect and stop invalid disputes before a chargeback can be filed. While these represent steps in the right direction, these products aren’t ideal solutions. For instance, let’s say a Visa cardholder disputes a transaction. If the buyer is intent on committing first-party fraud, no additional transaction information is going to change that decision.

Visa’s newest initiative — known as Compelling Evidence 3.0 — may prove more effective at stopping invalid chargebacks.

CE 3.0 is an updated set of guidelines and parameters which make a cardholder dispute invalid if specific compelling evidence can be provided to support the transaction. Under the new rules, merchants can resolve disputes by producing evidence of previous undisputed transactions from the same cardholder.

Through CE 3.0, merchants can keep many invalid disputes from becoming chargebacks. It’s a powerful evolution. But, is it enough to stem the growing threat of first-party fraud?

Compelling Evidence 3.0 only affects claims filed under Visa reason code 10.4 (Fraud/card-absent environment)

What Does Compelling Evidence 3.0 Do?

Under the legacy rules, contesting a cardholder’s claim of fraud involved tracking down compelling evidence and submitting it to the issuer. The bank would rule on whether the documentation was sufficient to reverse the claim.

Compelling Evidence 3.0 not only broadens the list of possible evidence, it can also initiate the process automatically on the merchant’s behalf. It takes most human decisioning out of the mix; if the qualifying information is correctly submitted, the claim is resolved automatically. The issuer can not initiate a chargeback using Visa reason code 10.4.

So what qualifications does Visa require for applicable evidence? Under the CE 3.0 rules, merchants must be able to provide record of at least two previous transactions that meet the following criteria:

Transaction Profile:

- Purchase made by the same cardholder as the disputed transaction

- More than 120 days old, but less than 365 days old

- Not previously disputed or flagged as fraud

The merchant must also provide two of four core transaction data elements. One of these must be either the IP address or the device ID. For the second transaction data element, the merchant may submit one of the following:

- Customer account ID

- IP address

- Device ID

- Shipping address

The process itself goes something like this:

Not only is the process made simpler, Visa claims that the merchant’s fraud and dispute ratios could be lowered by leveraging the new rules.

Does CE 3.0 Actually Prevent Chargebacks?

The short answer is “yes.”

Visa reports that up to 75% of disputes are friendly fraud. These claims could be blocked by issuers providing additional transaction details, which Compelling Evidence 3.0 facilitates. And, while it’s still a little early to get absolute figures, there’s good evidence to suggest that Compelling Evidence 3.0 will significantly reduce invalid chargeback issuances.

In the table below, we see the total number of disputes that were deflected per month using Order Insights. These are then compared to the number of disputes avoided per month when CE 3.0 is deployed. The difference is stark; however, the gap is likely to close as more and more merchants embrace CE 3.0:

| Month | Net Pre-Dispute Deflections | Pre-Dispute Deflections When CE 3.0 is Used |

| October 2023 | 3.4% | 50.4% |

| September 2023 | 3.6% | 49.9% |

| August 2023 | 3.7% | 50.6% |

| July 2023 | 2.9% | 42.6% |

| June 2023 | 3.3% | 27.7% |

To take full advantage of CE 3.0, though, merchants need to be integrated into the Order Insights platform. This is the only way to “prevent” a chargeback filed using reason code 10.4.

CE 3.0 rules can be applied after a chargeback has been filed. Merchants can submit the transaction data elements post-chargeback in order to have the chargeback reversed. But, these compelling evidence changes are most effective when used to keep disputes from becoming chargebacks in the first place. Blocking potential fraud at the inquiry stage not only lowers one’s fraud ratio and chargeback ratio; it also prevents the wasting of additional revenue while fighting invalid claims.

It’s also worth mentioning that some business models could benefit from the new initiative more than others. Merchants offering subscription services, for instance, will likely see the best results, as this model will make it easier to establish historical footprints and data validation.

CE 3.0 Is Good. Could It Be Better?

It should be noted that Compelling Evidence 3.0 is not a “silver bullet” for all first-party fraud.

As we mentioned, the new rules will be of more use to some business types than others. Leveraging CE 3.0 requires merchants to collect and store specific kinds of transaction data; possibly more than the retailer had been doing before. Plus, for pre-chargeback use, the merchant must be enrolled in Order Insight.

There are other limitations to CE 3.0 use. For example, it is currently only available for transactions between the cardholder and same merchant; cardholder activity across multiple unrelated businesses cannot be considered. Also, remember that CE 3.0 only applies to disputes that would’ve been filed using Visa reason code 10.4.

In certain situations, the type of evidence allowed may be subject to limitations, as well. For example, if an order has not been shipped, the delivery address cannot be used. As of this report, Visa does not consider biometric authentic data as part of the response data, although that may change. And since the system is based on historical data, any dispute initiated on a first-time purchase will obviously not qualify for CE 3.0 coverage.

Finally, CE 3.0 minimizes merchant involvement, but it won’t eliminate it. That’s where a comprehensive chargeback management strategy from Chargebacks911 can prove invaluable. Our experts can help you seamlessly tie CE 3.0 and Order Insight right into your workflow. Best of all, everything is accessed through a single user-friendly dashboard. If you're not enrolled in Order Insight yet, don't worry: as certified facilitators, we can help get you up and running quickly.

Visa Compelling Evidence 3.0 is a game-changer in the fight against first-party fraud. It will work best, however, as part of a multi-level fraud and chargeback management strategy. If you’re interested in learning how to gain the most advantage from CE 3.0, contact Chargebacks911® today.