Mastercard Chargeback Reason Code 4853: Cardholder Dispute

Mastercard Chargeback Reason Code 4853: Cardholder Dispute

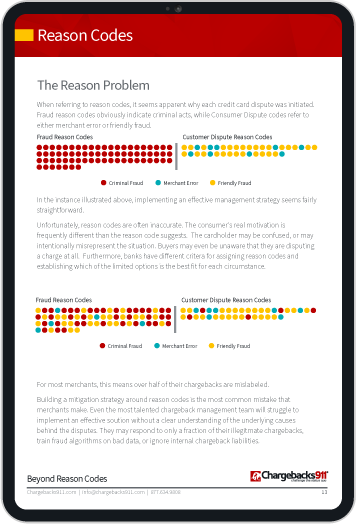

Mastercard chargeback reason code 4853: Cardholder Dispute refers to specific customer payment disputes involving transactions for goods or services. In this scenario, the customer has an issue, either with the transaction or the item itself, and does not believe the situation can be resolved through the merchant.

In some situations, Mastercard allows consumers to reverse a payment card transaction by filing a chargeback. To simplify this process, the scenarios that may qualify for a chargeback are broken down into designated “reason codes.” Banks assign the appropriate code to each case so everyone knows the given reason for the chargeback.

We say the given reason because it may or may not reflect the true reason. But, even if they suspect the cardholder is making an invalid claim, merchants must respond to the reason code presented by the bank.

The process is further complicated by the fact that each card network has its own set of reason codes. While most of the same scenarios are covered, the designations can vary considerably. Understanding which code is which can be challenging, so we’ve created guides to help merchants know how best to fight or prevent the different reason codes.

With that in mind, let’s take a look at Chargeback Reason Code 4853: Cardholder Dispute.

Should Merchants Worry About Reason Code 4853 Chargebacks?

Chargeback questions? We have answers. Click to learn more.

What Is a 4853 Chargeback?

Chargeback reason code 4853: Cardholder Dispute applies to situations in which a customer feels they have been cheated or misled. This broad umbrella category includes an array of chargeback causes. It could apply for merchandise or services being different than described, or disputes involving counterfeit goods (just to name a few examples).

Many of these causes had their own specific reason code at one time. Now, though, they’re bundled together under reason code 4853. So how does a merchant know which reason is being claimed for the chargeback?

When applicable, an additional message will be provided along with the reason code. Financial institutions refer to this as the Member Message Text, and it tells the merchant which particular type of chargeback applies to the claim.

Not all reason codes will require this supplemental information, but many do. The possible types that fall under the category of customer dispute chargeback are:

- Goods or services not as described or defective

- Goods or services not provided

- Digital goods purchase ($25 or less)

- Counterfeit goods

- Recurring transaction dispute (cardholder initiated)

- Recurring transaction dispute (issuer initiated)

- Addendum (unauthorized second charge)

- Transaction did not complete

- Credit not processed

- Credit posted as a purchase

Knowing the type of chargeback applied can help a merchant pinpoint the specific reason a customer dispute reason code was used. This information is crucial for disputing the chargeback, and for taking steps to prevent future claims of the same type.

Cardholder Disputes: Causes and Conditions

Legitimate reason 4853 chargebacks can come from a wide range of triggers. However, most typically result from merchant missteps, such as:

- Providing inaccurate descriptions or photographs

- Shipping the wrong product

- Not packaging merchandise securely for delivery

- Failing to ship orders or provide services as agreed

- Failing to make merchandise available for pickup as agreed

- Billing the cardholder prior to order delivery/receipt

Issuers have a limited timeframe to file chargebacks with a customer dispute reason code. Challenges must be processed within 120 calendar days of one of the following start dates:

- Transaction processing date

- Delivery date

- Cancellation date

- Date services ended (not to exceed 540 days of the original transaction processing date)

Also, in cases where the cardholder cancelled the service or returned the goods in question, issuers must wait at least 15 calendar days before initiating a dispute. Other conditions and different deadlines may apply; this depends on the exact cause being claimed in the chargeback, as well as where the transaction took place.

Cardholder Dispute Chargebacks and Fraud

Obviously, merchants can avoid most of the above situations by following best practices. Unfortunately, reason code 4853 is also commonly used to enable friendly fraud, or a consumer attempting to force an unearned refund through the bank.

As we noted earlier, the given reason for a chargeback may be completely different from the actual reason. The customer may be experiencing buyer’s remorse, or may want to avoid return shipping or restocking fees. Some customers may simply feel that filing a chargeback is easier than the merchant’s return process.

Whatever the true reason, claiming the order never arrived or was damaged is an easy excuse that banks understand. Merchants have the right to challenge these invalid claims through the representment process, and should do so.

Responding to Mastercard Reason Code 4853 Chargebacks

The good news is that most of these invalid claims are disputable by the merchant.

Take, for example, a reason code 4853 chargeback claiming that merchandise or services ordered were not received. If the merchant has a signature showing that the order was delivered, or evidence that the cardholder has used the service, there is a chance of getting the chargeback reversed. This is a process called chargeback representment; the merchant literally “re-presents” the transaction to the bank.

Representment is not an option with genuine customer dispute chargebacks, though. If the merchant is actually at fault, they have no choice but to accept the losses.

Merchants who suffer legitimate 4853 reason code chargebacks should focus on taking steps to tighten quality control and enhance customer service. This is the best way to prevent these chargebacks in the future.

Chargeback Management vs. Prevention

While merchants can take many steps to help prevent legitimate claims, friendly fraud is post-transactional in nature: there’s no sure way to identify it beforehand. Merchants can do everything “right,” yet still have a customer dispute chargeback filed against them.

Still, it’s generally more efficient to take a proactive stance when it comes to chargeback management. A truly effective strategy must encompass prevention as well as disputing cases of friendly fraud.

Chargebacks911® can help your business manage all aspects of chargeback reason codes, with proprietary technologies and experience-based expertise. Contact us today for a free ROI analysis to learn how much more you could save.