<cracking;the;code/>

REASON CODES

Chargeback Reason Codes: The Ultimate Guide

Understanding Chargeback Reason Codes is Key to Effective Chargeback Management

Every chargeback has something which triggers the initial dispute. Chargeback reason codes were created to standardize the list of acceptable reasons why a bank may file a credit card chargeback or debit chargeback on their customer’s behalf.

We've provided a breakdown here of the four major US-based schemes to help demonstrate the similarities and differences between the chargeback codes of different card networks.

Need to look-up a chargeback reason code? Use the widget above simply key-in your reason code and get a detailed explanation of what it means. Need more information? Keep reading to get the reason code rundown.

What is a Reason Code?

- Reason Code

A chargeback reason code is a 2- to 4-digit alphanumeric code provided by the issuing bank involved in a chargeback, which is meant to identify the reason for the dispute. Each of the major card brands, including Visa, Mastercard, and others, have their own system of reason codes.

[noun]/rēzən • kōd/

Reason codes are important to help you address recurring chargeback triggers. They can also help you identify invalid chargebacks and prepare a response.

Let’s assume that a cardholder, or the issuing bank acting on the cardholder’s behalf, decides to dispute a transaction. The bank files a chargeback and attaches a chargeback reason code to the case. You can then accept the dispute, or use the reason code to build a case with compelling evidence explaining why the original transaction was valid.

Having multiple lists for different card brands can be confusing. But, the chargeback justifications behind them remain pretty consistent across all networks. Whatever the reason code designation being used, the lists all serve the same basic purpose: to identify and describe the underlying motivation behind the transaction dispute.

Reason Codes by Card Network

There are numerous card brands throughout the world. Some are specific to certain regions or nations, while others are focused on specific industries like travel and entertainment cards, and each card scheme has their own system of chargeback reason codes. The four most widely-used in North America are Visa, Mastercard, American Express, and Discover.

We've provided a breakdown here of the four major US-based card networks to help demonstrate the similarities and differences between the reason codes of different card networks:

Visa Chargeback Reason Codes

Visa Chargeback Reason Codes are grouped into four categories: processing errors, authorization errors, fraud, and customer disputes. You’ll notice each category is denoted by a two-digit number, while the specific reason code is a subset of that group represented by a decimal place.

Learn more about Visa reason codes

Mastercard Chargeback Reason Codes

Mastercard has revamped their reason code list several times in recent years, condensing the list to modernize the Mastercard ecosystem. All Mastercard chargebacks active as of 2018 are denoted by a four-digit reason code beginning with a 48XX prefix.

Learn more about Mastercard reason codes

American Express Chargeback Reason Codes

The Amex list is divided into the same four subheadings used by Visa, along with an additional “Miscellaneous” category. The alphanumeric code uses a letter to denote the section, then a number for the specific reason; for example, “No Cardmember Authorization” is reason code F14; “F” for the “Fraud” category, and 14 for the specific claim.

Learn more about Amex reason codes

Discover Chargeback Reason Codes

Unlike the other three card networks, Discover uses a mostly alphabetic reason code system. Some of these reason codes are easy to recognize; for example, the reason code “DP” denotes “Duplicate Processing.” Others are less obvious, though, like “RM” for “Quality Discrepancy.”

Learn more about Discover reason codes

What Can Reason Codes Tell You?

Chargeback reason codes help merchants identify why they received a chargeback, what can be done to resolve it, and how to prevent similar disputes in the future.

Broadly speaking, most legitimate chargebacks can be traced to one of four sources: fraud, authorization issues, processing errors, or a customer dispute. You should take a period inventory of the chargebacks you receive to see if they fall disproportionately into one or more categories. You can then take corrective action to address recurring problems. For example:

Merchants who receive repeated chargebacks due to unauthorized transactions should perform a security overhaul. Fraud prevention or detection measures deployed at checkout, such as 3-D Secure, address verification services (AVS), and velocity checks, can help identify fraudulent activity.

If you receive chargebacks due to authorization issues or processing errors, you should have a chat with your payment service provider. See if any hardware, software, tools, or infrastructure shortcomings can be addressed. Or… maybe it’s simply time to switch to a new vendor.

If you receive chargebacks stemming from customer dissatisfaction, you should examine your product quality, customer service procedures, and general operations. Are shipments consistently delayed or packed incorrectly? Are your products of consistent quality? Are they marketed fairly and honestly?

This analysis will help you enhance product quality, improve on-time delivery rates, speed up customer service response times, and reduce packing errors. In turn, this will help you strengthen customer satisfaction and keep your chargeback rate at an acceptable level.

You can use chargeback reason codes to determine which chargebacks to fight as well. If you receive a chargeback, but the reason code doesn’t accurately reflect the transaction. Then you can submit a response through the representment process.

The reason code will also provide guidance on the kind of compelling evidence needed to win a chargeback reversal.

When Reason Code ≠ Reason

A growing number of chargebacks are filed without a valid reason for a dispute. In these cases, you cannot trust the reason code to give you an accurate impression of the situation.

The goal behind the chargeback reason code system is to eliminate guesswork and opinion-based decisions. All parties can refer to the reason code and understand the issue that caused the chargeback. Issuing banks don't have to justify their decisions, and acquiring banks and merchants know what specific documentation they need for representment.

For the most part, the process works…at least for legitimate chargebacks. The problem: not all chargebacks are legitimate.

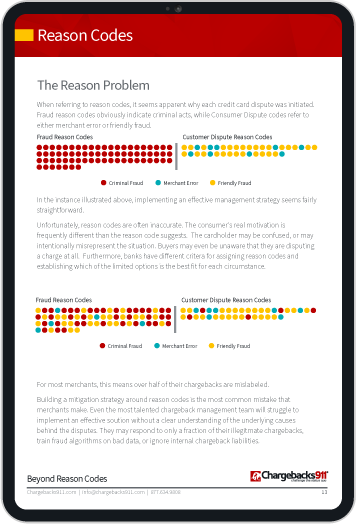

Established chargeback reason codes do a good job of addressing processing errors, merchant fraud, and other “legitimate” reasons for filing a dispute. But as research shows, more and more chargebacks are being filed for reasons that have little to do with the assigned chargeback code.

The real motives behind these disputes, such as buyer's remorse, family fraud, or an unwanted item that has gone beyond the return date, are not considered legitimate chargeback reasons. As such, they have no code. However, many customers do an end run around the problem by claiming that the transaction is fraudulent. This is a practice known as “friendly fraud.”

There are cases where friendly fraud might be an accident or a simple misunderstanding. But, most merchants view this technique as a way of getting something for free: in other words, shoplifting.

Fighting Fraudulent Reason Codes

You can respond to chargebacks through the representment process. This involves gathering evidence and resubmitting the transactions along with additional documentation.

Figures in the 2024 Chargeback Field Report reveal that more than 50% of all chargebacks are filed for illegitimate reasons. When this happens, merchants are saddled with fees that can range between $20 and $100 per claim.

Luckily, you have some recourse: invalid chargebacks can be challenged through representment. This is a strict and highly regulated process that gives you an opportunity to present compelling evidence and rebut the cardholder’s claims. That said, the odds are not in your favor: although sellers win 45% of the disputes they re-present on average, they recover revenue in only about 18% of cases.

Still, it’s considered best practice to re-present all fraudulent disputes. You can do this by following the steps below:

#1 | Identify the Chargeback Reason Code and Response Time Window

As we’ve mentioned earlier, chargeback reason codes help you understand what kind of evidence and rebuttal you can most effectively furnish in representment.

Prior to compiling a representment package, you should be aware that you will need to work under tight deadlines. The card network will typically allow 20-45 days to respond. Your acquirer, however, may be less generous; some banks give as little as five days to draft a response. So, you should get to work as soon as you receive a chargeback.

#2 | Gather Compelling Evidence

Now, it’s time to gather convincing evidence based on the chargeback reason code, the issuing bank, and the card network. For example, the evidence you submit to challenge a non-delivery chargeback claim could include shipping details, a copy of the parcel’s tracking information, buyer signatures at the point of delivery, and receipts and invoices associated with the purchase.

#3 | Write a Strong Rebuttal Letter

This one-page document should summarize why the cardholder’s claim is invalid, why the transaction should be upheld, and why the merchant’s evidence-based argument is correct. The letter should also contain identifying information, such as the merchant’s name, contact information, transaction ID, and the product/service sold. It’s also best practice to provide the chargeback reason code and case number, the acquirer reference number, and the amount under dispute.

#4 | Submit Your Representment Package

Finally, compile your documents and submit them to your acquirer, who will forward it to the issuer. Remember that you must submit your representment package within the timeframe set by the card network, and that your evidence must comply with card network and issuer guidelines. Specifically, Visa and Mastercard require evidence to be in PDF or JPEG file formats. In addition, Mastercard accepts no more than 10 megabytes (MB) of evidence, while Visa permits only 2 MB worth of uploads.

Need More Help?

You can’t implement a consistent and effective chargeback prevention strategy unless you can identify the true cause of chargebacks.

Chargebacks911® offers the first tool ever developed to make this a reality: Intelligent Source Detection™.

Our Intelligent Source Detection will identify the true chargeback triggers affecting your business, and help you understand the reason behind the chargeback reason codes. Contact us today for a free ROI analysis. We’ll show you how much more you can earn by accurately identifying chargeback causes, implementing an effective prevention strategy, and disputing illegitimate chargebacks.

FAQs

What are the reason codes for chargebacks?

Chargeback reason codes communicate the reason a dispute was filed. Although chargeback reason codes across different card networks vary in style and naming convention, they communicate the same chargeback reasons. Broadly speaking, these include authorization issues, fraud, processing errors, point-of-interaction errors, and cardholder disputes.

What is a valid reason for a chargeback?

Cardholders who are victims of fraud or unauthorized activity can file valid chargebacks, as can customers who receive defective, damaged, missing, counterfeit, or severely delayed goods. Cardholders can also file valid chargebacks if they are billed incorrectly or more than once.

Can I chargeback for any reason?

No. Unless you received defective, damaged, or missing goods, or were a victim of fraud, unauthorized activity, or a merchant billing error, you do not have a legitimate reason to file a chargeback. If you file a chargeback for an invalid reason, you risk committing first-party misuse, friendly fraud, or chargeback fraud.

What makes a chargeback invalid?

A chargeback is invalid when a cardholder initiates one for an illegitimate reason. Buyer’s remorse, the desire for a quick refund, misidentifying the merchant’s billing descriptor, or the urge to get an item for free are all invalid reasons to file a chargeback.

How do you win a chargeback dispute?

Cardholders do not have to do anything to win a chargeback dispute. Once filed, the issuer investigates the claim and handles the process from there. Merchants who wish to win chargebacks must engage in the representment process, which is a strict and tightly regulated process that gives sellers the opportunity to prove that the chargeback is invalid and request that it be reversed.

Do merchants usually fight chargebacks?

Merchants typically fight most or all invalid chargebacks, especially if they have evidence to show that the cardholder is in the wrong. However, merchants may leave valid chargebacks unchallenged, since winning those are unlikely, if not impossible.

Confused By Chargeback

Reason Codes?

Download our convenient quick reference

cheat sheets