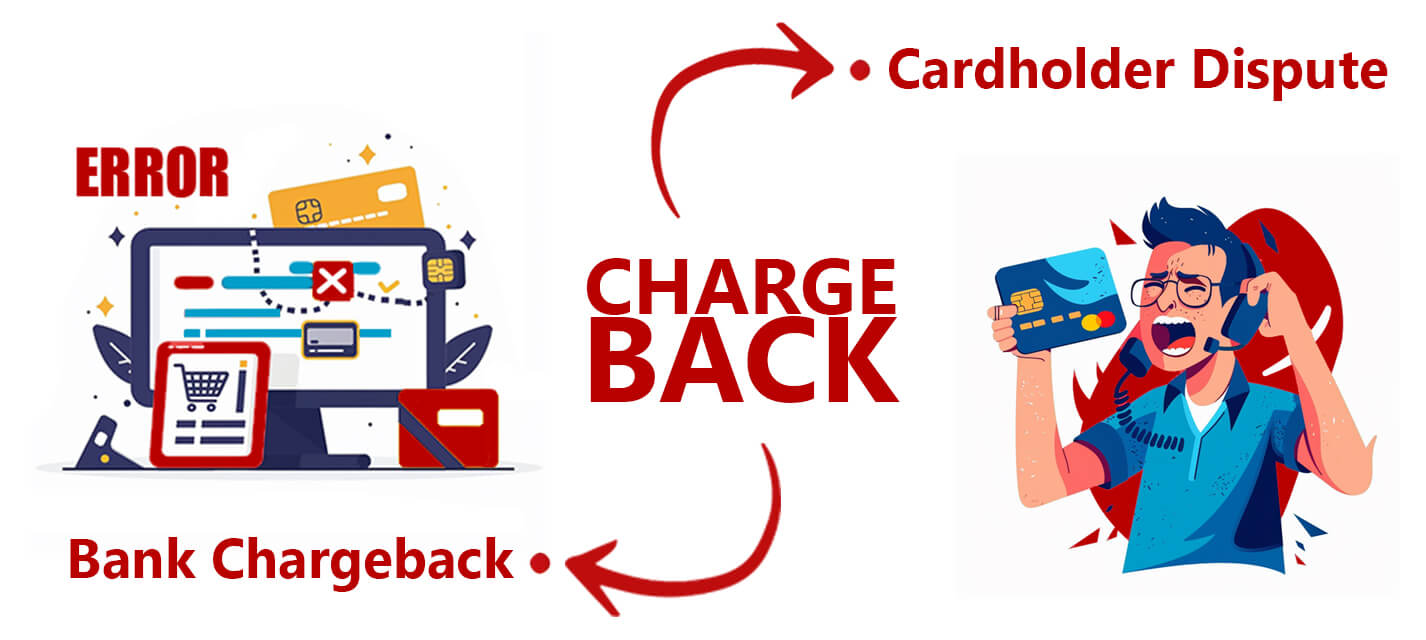

What is a Bank Chargeback? What Makes it Different From Other Disputes?

Bank chargebacks are disputes initiated by a cardholder’s issuing bank.

The motivations and processes involved are different from a conventional customer dispute. But for you, as a merchant, the end result can seem largely the same: lost revenue, added fees, and a higher chargeback rate.

So, what’s different about a bank chargeback? What causes these disputes, and what’s the difference between a bank chargeback and a regular chargeback?

Recommended reading

- Bank of America Disputes: Here's What You Need to Know

- Wells Fargo Disputes: Chargeback Rules & Things to Know

- 10 Tips to Stop DoorDash Chargebacks Before They Happen

- American Express Chargebacks: Rules & Time Limits & More

- Stripe Chargeback Guide: Time Limits & Other Info You Need

- Card-Not-Present Chargebacks: The Merchant's Guide for 2024

How Bank Chargebacks Differ From Cardholder Disputes

With a standard chargeback, a transaction reversal occurs because some part of the process went wrong or was incorrect.

The “something” that went wrong could be anything from a technical glitch to an error or a fraud claim. In many cases, though, the claim is initiated by the cardholder. A bank chargeback, on the other hand, is initiated by the issuer, not the customer.

A bank chargeback happens when the issuer detects some anomaly in the transaction process. And, true to their name, bank chargebacks can often be handled at the banking level. The issuing bank and the acquiring bank often work to resolve these disputes between themselves. Both the buyer and the seller may be completely unaware that a chargeback is being processed.

When all is said and done, however, we’re still talking about a chargeback. That means that, at some point, the claim will be settled. In most cases, the funds will be transferred from your account to the cardholder, just the same as with any other dispute.

What Counts as a Transaction Anomaly?

Bank chargebacks are typically triggered by an error in the original transaction. Something in the transaction is “off” in some way. It may or may not actually be causing an issue, but it at least has the potential to create trouble.

The most common causes of bank chargebacks include:

Some of these anomalies may seem benign, but the bank may file a chargeback anyway. From their perspective, they’re just being proactive; they see a bank chargeback as a way to protect themselves — and their customers — from future trouble.

For example, say a transaction uses an account number that doesn't match the number on file with the issuer. There might be a legitimate reason for this. But, the issuer doesn’t know that. Rather than take a chance, the bank files a chargeback “just in case.”

Practical Examples of Bank Chargebacks

What do transaction anomalies look like in the real world? Here are three commonplace scenarios that can better illustrate how a simple transaction can raise red flags and lead to bank chargebacks:

Scenario 1 | Expired Card Transaction

Sarah owns a bookstore. One busy afternoon, a tourist steps in, picking up a handful of books before heading to the counter. The customer’s card doesn’t work in the card reader, and there’s a rush of customers at the moment, but Sarah doesn’t want to miss out on the sale. She rushes to key in the information manually, but fails to check the expiration date on the tourist's credit card.

The card, unbeknownst to both Sarah and the tourist, had expired the previous month. The transaction seems to go through without a hitch, and the tourist leaves happy. However, when the bank conducts its routine check, it flags the transaction due to the expired card. The bank, prioritizing protocol and security, initiates a chargeback against the bookstore, leaving Sarah puzzled and concerned about how such an oversight occurred.

Scenario 2 | The Duplicate Processing Dilemma

Mary runs a boutique coffee shop in the city. One day, a regular customer named Joe comes in for his usual espresso and box of pastries before heading into the office. They chat about the day as Mary prepares the coffee, and Joe hands over his card for payment. The point-of-sale system, however, glitches momentarily. Mary is unsure if the transaction went through, so she swipes the card again.

The bank's systems, designed to detect such discrepancies, pick up on the duplicate transaction. Even without a direct complaint from Joe, the bank decides to issue a chargeback for the second charge, recognizing it as an error in processing.

Scenario 3 | Late Presentment Leads to Trouble

Michael owns a small online gadget store. He's meticulous with orders, but occasionally gets overwhelmed due to the volume of sales. During a particularly busy period, when Michael is swamped with fulfilling orders, he delays submitting transaction details to the bank. A customer's purchase goes through smoothly, and the item is delivered on time. However, Michael forgets to present the transaction to the bank for several days after the purchase.

Upon reviewing transactions, the bank notices the delay in presentment. Even though the customer has not raised any issues with the purchase, the bank initiates a chargeback against Michael's store for failing to comply with the terms of timely transaction processing.

Each of these scenarios underscores the critical nature of adhering to payment processing protocols and the unexpected challenges merchants can face when these protocols are overlooked.

Can Merchants Fight Bank Disputes?

As we mentioned, bank chargebacks are much harder to fight than customer disputes. If you have evidence that a customer dispute was invalid, you can challenge the chargeback through representment.

Outside of a technical fault, however, it’s rare that the issuer will reverse a bank chargeback. Banks typically initiate chargebacks based on their assessments and findings, so reversing their decision requires a compelling, undeniable case. Unfortunately, it's relatively rare for a bank to change its stance after issuing a chargeback, except in cases where the merchant can provide incontrovertible evidence to support their claim.

Representment offers a path to dispute chargebacks. But, you should still manage your expectations and focus primarily on preventative measures to minimize the risk of chargebacks occurring in the first place. Luckily, most bank chargebacks are the result of simple missteps on the merchant’s part, which means they’re nearly 100% preventable.

10 Ways to Prevent Bank Chargebacks

Self-examination is one of the most challenging — yet crucial — actions you must take to eliminate internal chargeback triggers. An exhaustive, unflinching evaluation of your business is the only way to identify policies and practices that create problems.

Seemingly minor errors can lead to significant revenue loss. One of the best ways to reduce risk is to take a fresh look at your policies and procedures. Make sure you’re following proven best practices for accepting payment cards in card-not-present situations:

#1 | Strict Adherence to Network Rules

Familiarize yourself with, and rigorously follow, the rules set by credit card networks. This includes understanding the requirements for transaction processing, dispute resolution, and compliance standards to avoid violations that could lead to chargebacks.

#2 | Get Authorization for Every Transaction

Always obtain authorization for every transaction to confirm the cardholder's bank approves the sale. Attempting to process transactions without proper authorization, or trying to bypass a declined card, significantly increases the risk of chargebacks.

#3 | Efficient Order Fulfillment

Develop a system for packing and shipping purchases promptly. Delayed shipments can lead to customer dissatisfaction and chargebacks. A streamlined fulfillment process not only enhances customer satisfaction but also reduces the likelihood of disputes related to shipping delays.

#4 | Prompt Credits & Cancellations

Implement a policy to process refunds, credits, and cancellations swiftly once requested by a customer. Delaying refunds or making it difficult for customers to cancel services can lead to chargebacks as customers turn to their banks to resolve their grievances.

#5 | Timely Deposit of Sales & Credit Receipts

Make sure all sales and credit receipts are deposited with your processing bank within one to five days of the transaction date. Adhering to this timeframe helps maintain accurate financial records and prevents discrepancies that could lead to chargebacks.

#6 | Verify Shipment Before Deposit

Confirm that merchandise has been shipped — and preferably received by the customer — before depositing the funds from a transaction. This practice helps avoid chargebacks related to claims of non-receipt of goods.

#7 | In-Depth Self-Examination

Conduct regular and thorough reviews of your business operations, customer service practices, and transaction processing procedures. This self-examination should aim to uncover any internal triggers for chargebacks, such as unclear billing descriptors, inadequate customer service, or lax fraud prevention measures.

#8 | Enhanced Fraud Detection Tools

Utilize advanced fraud detection and prevention tools, such as address verification service (AVS), card verification value (CVV) checks, and two-factor authentication for online transactions. These tools help verify the identity of the cardholder and reduce the risk of fraudulent transactions.

#9 | Clear Communication & Transparency

You need to be sure that all communication with customers is clear, especially regarding product descriptions, terms of service, and return policies. Transparency in business practices builds trust and reduces misunderstandings that can lead to chargebacks.

#10 | Detailed Record-Keeping

Keep detailed records of all transactions, customer communications, and documentation related to shipments and refunds. Comprehensive records can be invaluable in disputing chargebacks by providing strong evidence to support your case.

Even with the best intentions, it’s hard to take a completely unbiased look at your own operation. If you find you need help from an external source, Chargebacks911® offers the solution.

Our proprietary services are designed to identify hidden chargeback triggers that are costing you money. Don’t fall victim to another bank chargeback. Contact Chargebacks911 and learn how a professional assessment can save you time and revenue today.

FAQs

Does chargeback mean refund?

No. Chargebacks and refunds are different things. A chargeback is a forced transaction reversal initiated by the cardholder's bank, often due to a dispute or suspected fraud, which can involve additional fees and penalties for the merchant.

Can a chargeback get you in trouble?

In a way, yes. Merchants can face penalties, fees, and potentially lose their ability to process payments if they receive too many chargebacks, as it indicates a high level of disputed transactions which can be seen as a risk by payment processors and banks.

What happens when a chargeback is issued?

When a chargeback is issued, the merchant's account is debited for the transaction amount, plus any associated fees, and the customer receives a refund from their bank. The merchant then has the opportunity to dispute the chargeback if they believe it was unjustified.

Should I accept a chargeback?

Accepting a chargeback may be a good idea if you know an error or fraudulent transaction occurred. However, if the chargeback is unjustified, you should consider re-presenting it, along with appropriate evidence.