Lots of Big eCommerce Changes are in Store…Are You Ready?

2018 is a big year for eCommerce…and for acronyms.

We’ve talked about VCR, GDPR, and PSD2 on our blog before, but we can’t overlook just how important these three updates are. Is your business really prepared for these revolutionary new processes? What are these new policies, and how can you tell if you’re ready to adapt?

VCR: Visa Claims Resolution

VCR: Visa Claims Resolution

Visa Claims Resolution went live on April 15, 2018. VCR marks a complete overhaul of the chargeback process, taking more than four decades of chargeback rules and protocols and throwing them out the window.

Now, all Visa disputes are filed into one of two workflows: allocation or collaboration. The former relies on automated processes to assign liability to the merchant, bank, or customer in a dispute. Collaboration, on the other hand, uses a litigation-based model like the existing representment process.

VCR is meant to save time and resources for everyone involved…but unfortunately, it’s not quite that simple. The process is much more of a “mixed bag.”

Reliance on automated systems can produce errors, especially when most chargebacks are caused by friendly fraud, rather than merchant error or criminal fraud. Plus, while merchants never had much insight into their chargebacks, the automated workflows implemented under VCR make the process even hazier. Lastly, new processes introduce uncertainty. We don’t know how VCR will impact the eCommerce environment years down the road.

Beyond VCR: Surveying the Impact of Visa Claims Resolution

We asked a wide range of merchants about the effects they are seeing from Visa's VCR initiative. Download your copy of our report to see what our research uncovered.

Free Download PSD2: Revised Payment Services Directive

PSD2: Revised Payment Services Directive

The Revised Payment Services Directive was first adopted by the EU Parliament in 2015, but finally went live in January 2018. Even if you’re not located on the continent, the PSD2 still applies to so-called “one-leg transactions,” or sales in which one party is in the EU. If you do business with any customers there, then the rule applies.

In short, the PSD2 allows tech companies like Facebook and Google to offer financial services like integrated bill pay, funds transfers, and more. Advocates claim this will free up the market and open card schemes like Visa and Mastercard to greater competition. At the same time, the rule means industry standards will be even less consistent than before.

Since these are not credit or debit transactions, chargeback rules under the Fair Credit Billing Act do not apply. Many PISPs (“payment industry service providers”) like iDeal do not allow chargebacks on their platform. That sounds great if you’re working with one of these systems…until you realize that you’ll have to separate these transactions from chargeback-liable credit and debit sales for recordkeeping purposes.

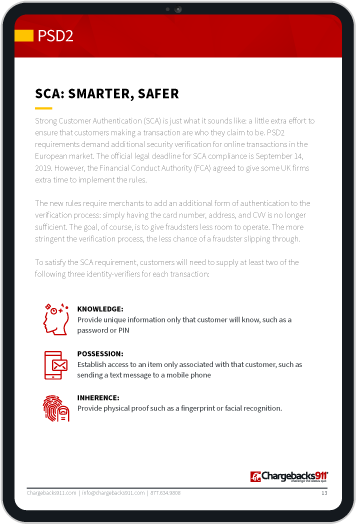

The PSD2 also mandates 2-factor authentication in card-not-present sales. While 2FA is a good idea, mandating it strips you of some autonomy in building your own, customized fraud solution.

GDPR: General Data Protection Regulation

GDPR: General Data Protection Regulation

The GDPR is another EU rule change, effective May 25, 2018. Like the PSD2, this regulation applies to “one-leg” transactions, so you will need to comply if you want to do business with any European customers.

The GDPR is meant to put power in the hands of consumers to govern how their data is used. It establishes mandatory consent, as consumers must opt-in before you can use data for any purpose not explicitly outlined in the terms of service. Even more important, it gives all EU citizens the “right to be forgotten,” meaning any data held by businesses must be easy-to-recall and destroy if the customer requests it.

This presents numerous logistical challenges. First and foremost, tracking where all that data is located is going to be a nightmare. Then there are less-obvious problems, like the fact that it will be extremely difficult to self-manage chargebacks with incomplete samples and datasets.

If EMV’s rocky adoption is any signal of how industry transitions pan out, then the entire global market is in for a rough experience as GDPR becomes more entrenched.

Trouble Keeping Up?

See how Chargebacks911® can push you one step ahead of the eCommerce curve.

We’ve Got Your Back

New policies, new technologies, but still the same old problem: how do you minimize costs and maximize revenue? Just one answer: Chargebacks911®.

Our revolutionary lineup of services offers everything you need to make these and future policy changes work for you:

Fighting chargebacks is just one part of what we do at Chargebacks911. Our services offer what no other service provider in the market can: true, proven chargeback reduction. You don’t need to worry about new rule changes; our solutions ensure that your chargebacks stay low.

How is that even possible? Click below and find out.