Excessive Chargeback Programs: Here's Everything Merchants Should Know

Credit card chargebacks are nothing but bad news for merchants.

Even a single chargeback can hurt your bottom line. That said, excessive chargeback levels can—and have—put many merchants out of business completely. This raises the question: how many is too many?

Customer disputes are more expensive than they seem at first glance. Our internal data suggests that, by 2023, the average chargeback will cost $191. This is based on a $90 average disputed transaction.

Even a few chargebacks can be a problem. Excessive chargeback levels, however, can send your costs through the roof, threatening both card-processing privileges and your ability to even function in the eCommerce environment.

In this post, let’s break down the idea of excessive chargebacks. We’ll see what the term means, how your chargeback ratio fits into the picture, chargeback monitoring, and what happens if you receive an excessive number of disputes.

Recommended reading

- Merchant Account Reserves: What You Need to Know in 2024

- High-Risk Merchant Accounts: The Best Providers of 2024

- What is a High-Risk Business? Why Does it Matter?

- How the Terminated Merchant File Can Affect Your Business

- Visa Dispute Monitoring Program: What is the VDMP?

- Basis Points: What Do They Say About Your Financial Health?

What is an Excessive Chargeback Rate?

“Excessive chargebacks'' seems like a vague, generic description. In this context, however, “excessive” means exceeding a specific threshold set by one of the card networks.

These thresholds can seem overly-harsh. However, they’re not designed to punish anyone. Instead, they’re meant to help card networks and banks assess financial risk posed by individual merchants.

The chargeback threshold is compared against the merchant’s chargeback rate. This is a calculation that measures the number of chargebacks your business receives within a month against the total number of transactions processed in that period.

Learn more about chargeback ratesWhile the figure outlined above is the general formula, it’s important to note that each of the four major card networks has its own way of calculating an acceptable ratio.

For illustrative purposes, we’ll focus on processes of the two largest schemes, Visa and Mastercard. We’ll touch on how they calculate ratios, how they define excessive, and the different monitoring programs they operate.

Excessive Visa Chargebacks

Let’s start by looking at the excessive chargeback thresholds set by Visa.

One thing to keep in mind here is that Visa uses different terminology than the other networks. The term “dispute” is used in place of chargeback, for example. Ultimately, though, “excessive Visa disputes” and “excessive Visa chargebacks” refer to the same thing.

How to Calculate Your Visa Chargeback Ratio

To find your Visa chargeback rate, start by taking the number of disputes filed against you in the current month. Then, divide that number by the total number of purchases you processed in the current month:

Visa Excessive Chargeback Limit

For Visa, an unacceptable chargeback level is a matter of degrees. If you breach certain thresholds, you could be entered into the Visa Dispute Monitoring Program, or VDMP. The company has established thresholds for three VDMP tiers: the “early warning,” “standard,” and “excessive” tiers.

Each tier is based on two criteria: your chargeback ratio, and the total number of chargebacks you received in that same month.

Learn more about Visa chargeback thresholdsVDMP: The Visa Excessive Chargeback Program

Being labeled as an “excessive chargeback merchant” in the Visa network means that the company identifies your recent activity as risky. This determination is based on how many chargebacks have been filed against you.

As you would expect, breaching the “early warning” threshold won’t have as much impact as going over the standard threshold, and crossing the threshold for the “excessive” tier has the harshest penalties. Unlike the other levels, the excessive dispute tier offers no grace period. Fines start immediately, and continue until you are removed from the program, or your account is canceled by the bank.

Chargeback processes and requirements change like the weather. It’s almost impossible to keep track … so let us do it for you.

For merchants with excessive Visa chargebacks, the enforcement period is 12 months. While in the program, merchants are also subject to a $50 fee for each dispute fee. Your acquirer will deduct the amount directly from your account.

Those fees are minimal, however, compared to the review fees merchants face. With both the regular and the excessive program, you’ll be subject to a $25,000 review fee toward the end of your 12-month enforcement period.

Learn more about VDMPCommon Question

Does Visa have a monitoring program specifically for fraud?

Yes. Visa also has a monitoring system in place for merchants who generate an excessive level of fraud activity. The Visa Fraud Monitoring Program (VFMP) is similar to VDMP, but covers more than just disputes.

Excessive Mastercard Chargebacks

Mastercard handles excessive chargebacks in a way very similar to Visa. That said, small differences, such as the way the chargeback rate is calculated, can cause confusion.

How to Calculate Your Mastercard Chargeback Ratio

To find your Mastercard chargeback rate, start with the number of first chargebacks filed in the current month. Then, divide this by the number of purchases made in the previous month.

Mastercard Excessive Chargeback Limit

Mastercard’s threshold for excessive chargebacks is split into two categories: Excessive Chargeback Merchant (ECM), and High Excessive Chargeback Merchant (HECM). Merchants are given one label or the other based on breaching predetermined monthly chargeback thresholds:

| Number of Monthly Chargebacks | Monthly Chargebacks (% of Total Transactions) | |

| Excessive Chargeback Merchant Program | 100 to 299 | 1.5% to 2.99% |

| High Excessive Chargeback Merchant Program | 300 or more | 3% or more |

ECM: The Mastercard Excessive Chargeback Program

Getting placed in either tier of the Mastercard Excessive Chargeback Program means that accepting payment cards will cost you more than ever. The penalties for both programs increase based on the number of months that you remain above the Mastercard chargeback threshold.

Mastercard also requires that banks submit monthly reports on the activity of each listed merchant. The network charges between US $50 and $300 per report. That said, the price of failing to file the reports is even worse, costing as much as US $1,000 per day, per report.

Mastercard might even mandate a costly action-plan review. In worst-case scenarios, you could be looking at non-compliance fees of up to $50,000 per month.

These fees are levied against the acquirer. But, they will almost certainly be passed on to you, along with a healthy mark-up. Also, while the enforcement period is 12 months, you won’t be immediately removed from the program just because your chargeback rate drops to an acceptable level. You’ll need to keep it under the threshold for three consecutive months.

Learn more about the ECM ProgramOther Consequences of Excessive Chargebacks

Even though the networks keep an eye on things, acquirers are expected to monitor chargeback rates as well. Acquiring banks get slapped with fees if one of their merchants’ accounts receives too many chargebacks.

The networks prefer this hands-off approach, but they will step in if the acquirer doesn’t act on a risky account. Rather than risk this oversight, most acquirers will decide it’s more cost-effective to simply terminate your account.

A terminated account means you lose the ability to process credit card payments. It will also likely land you on the MATCH list. This is a type of “blacklist” that acquirers use when determining the risk of taking on a new merchant.

Learn more about the MATCH ListAt that point, you’ll be forced to work with a high-risk payment processor. Of course, that’s assuming you can find a processor at all. The elevated fees associated with being high-risk create even more challenges for a business already struggling to survive.

Learn more about high-risk processingWhy Do Merchants Get Punished for Excessive Chargebacks?

As a merchant, it might feel like you’re getting a raw deal here. But, like we mentioned above, none of these enforcement methods should be considered a punishment.

Visa, Mastercard, and the banks don’t want to “punish” merchants for chargebacks. Instead, their purpose is to incentivize merchants to implement a plan for reducing disputes.

The bank may consider this self-preservation. For them, losing a merchant account here and there is better than being at odds with the card networks. At the same time, the card networks think of this as a way of ensuring brand integrity. By watching for merchants who receive excessive chargebacks, they’re hoping to maintain consumer confidence in the use of payment cards.

Where Excessive Chargebacks Come From

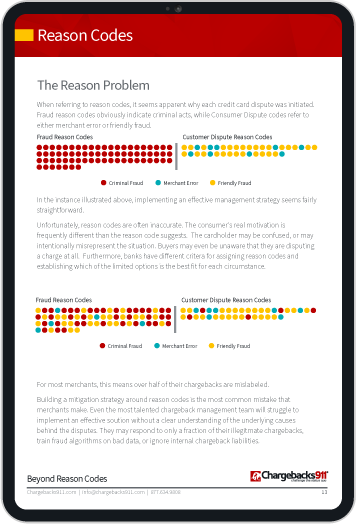

The chargeback system is not inherently bad. In fact, chargebacks are a much-needed form of consumer protection. They offer security to consumers who are victimized by criminal fraud or abusive practices.

That said, research conducted by Chargebacks911® has found that more than 60% of all chargebacks are probably cases of friendly fraud. This occurs when a consumer calls the bank for a chargeback without trying to obtain a refund first.

In theory, this means you could be effectively preventing criminal chargebacks, but still receive an excessive number of disputes. You end up taking a financial hit for someone else’s activities.

Learn more about chargeback sourcesBalancing the Scales of Friendly Fraud

So, how can you help tip the scales in your favor?

Consistently disputing illegitimate chargebacks is the best way to encourage industry-wide change. Chargeback representment is a costly, time-consuming process, though. Even a successful reversal doesn’t improve your chargeback ratio, as it only takes first chargebacks into account. Plus, if it’s not done properly, fighting friendly fraud can end up costing more money, aggravating customers, and alienating banks.

Most merchants simply don’t have the experience or expertise necessary to successfully navigate the chargeback process. There’s good news, though: help is available.

Chargebacks911® offers comprehensive, end-to-end chargeback management that covers prevention, management, and revenue recovery. We can help you make a stand against friendly fraud, and work your way back from the abyss of excessive chargebacks.

We can take chargeback management completely off your plate, dramatically increase your ROI, and leave you with more time to concentrate on your business.

If excessive chargebacks are a problem you need to address, contact us today for a no-cost ROI analysis.